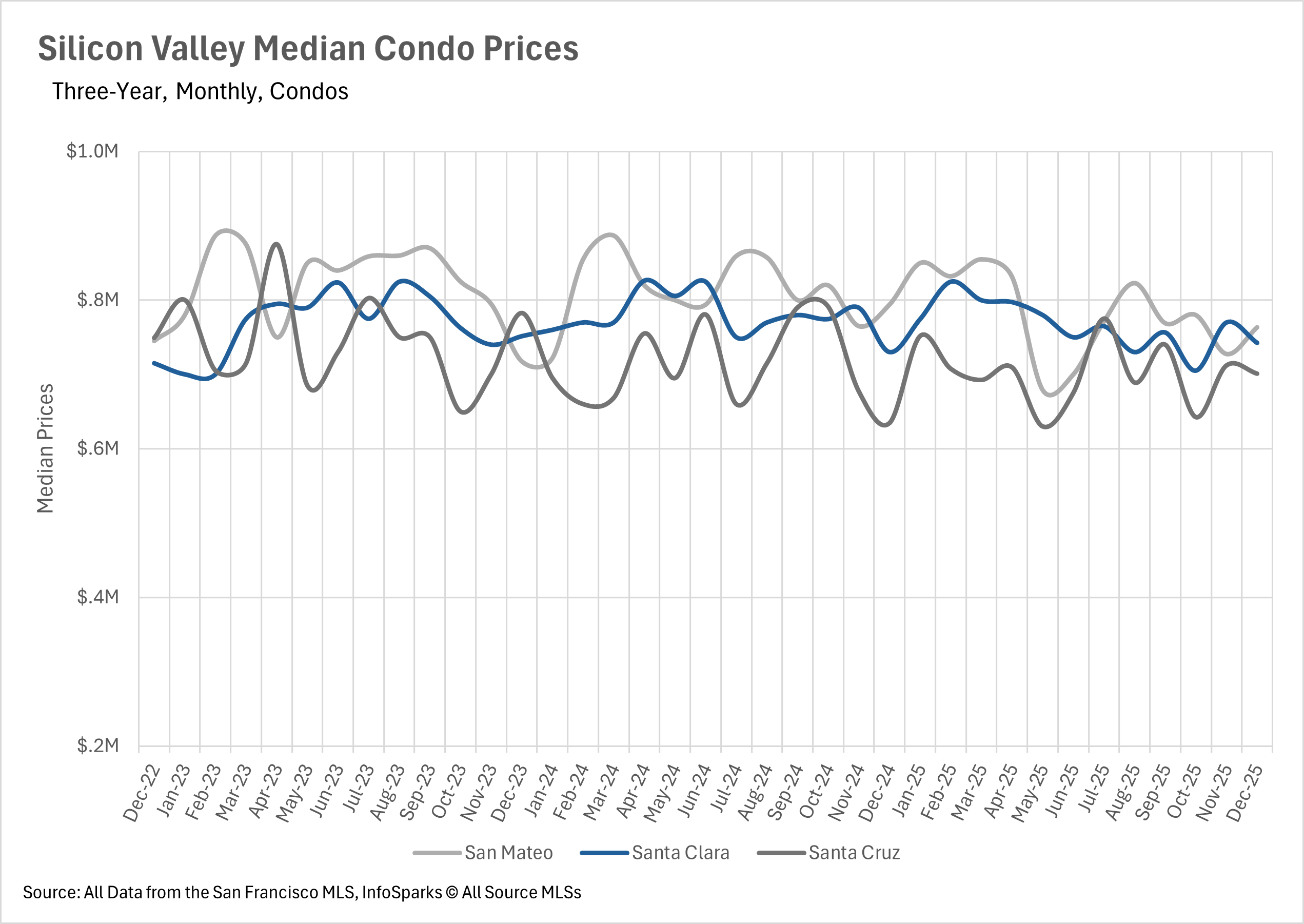

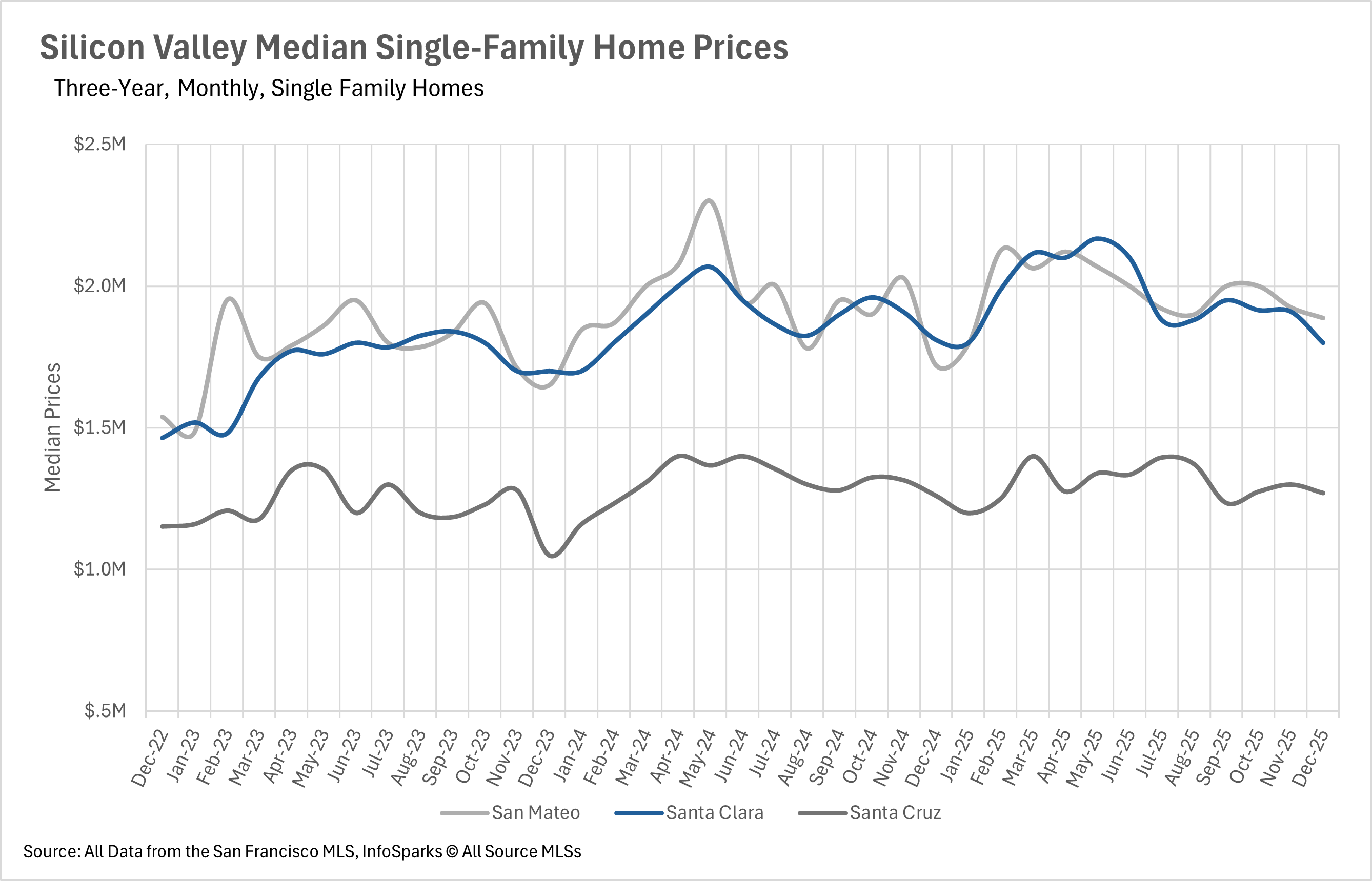

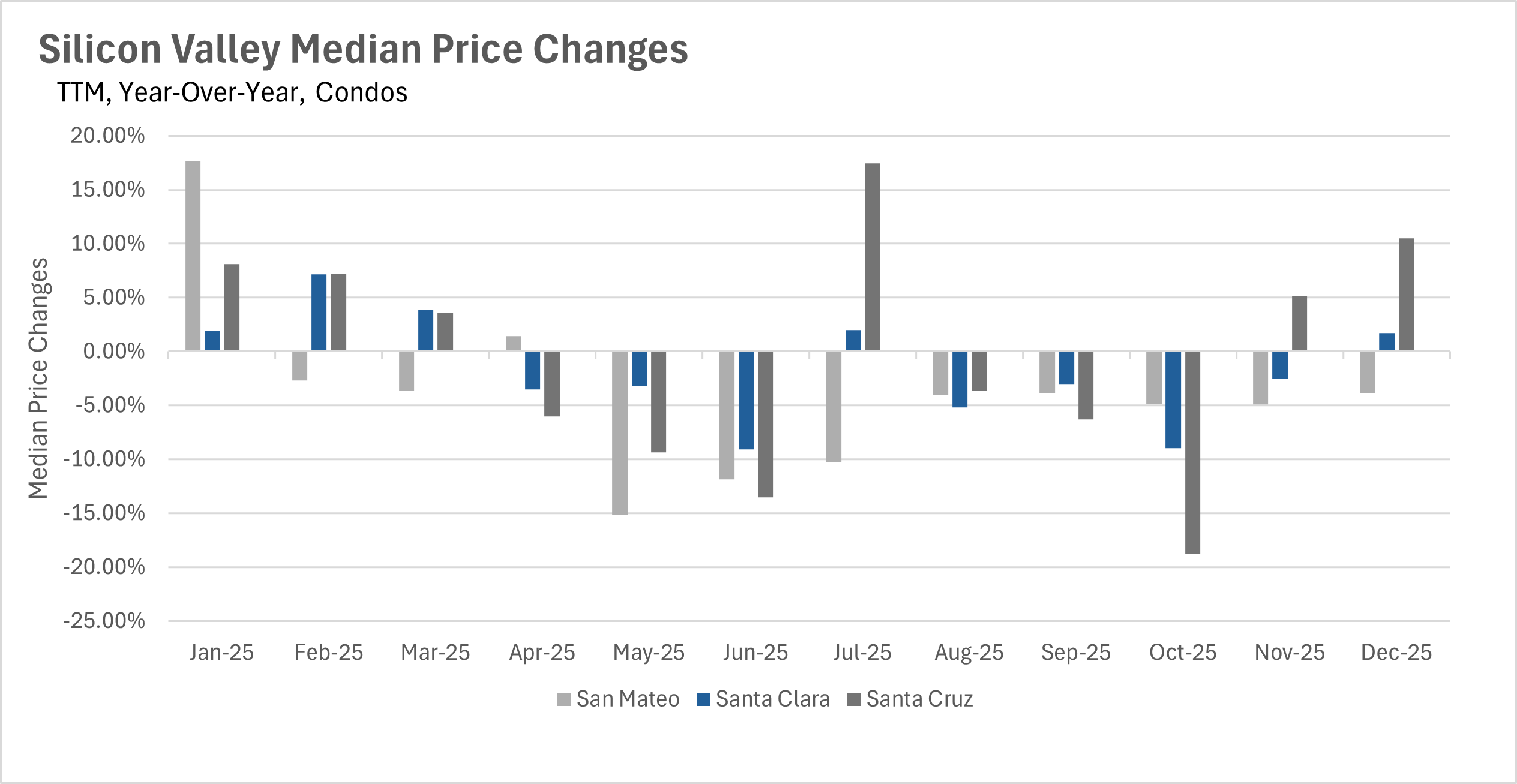

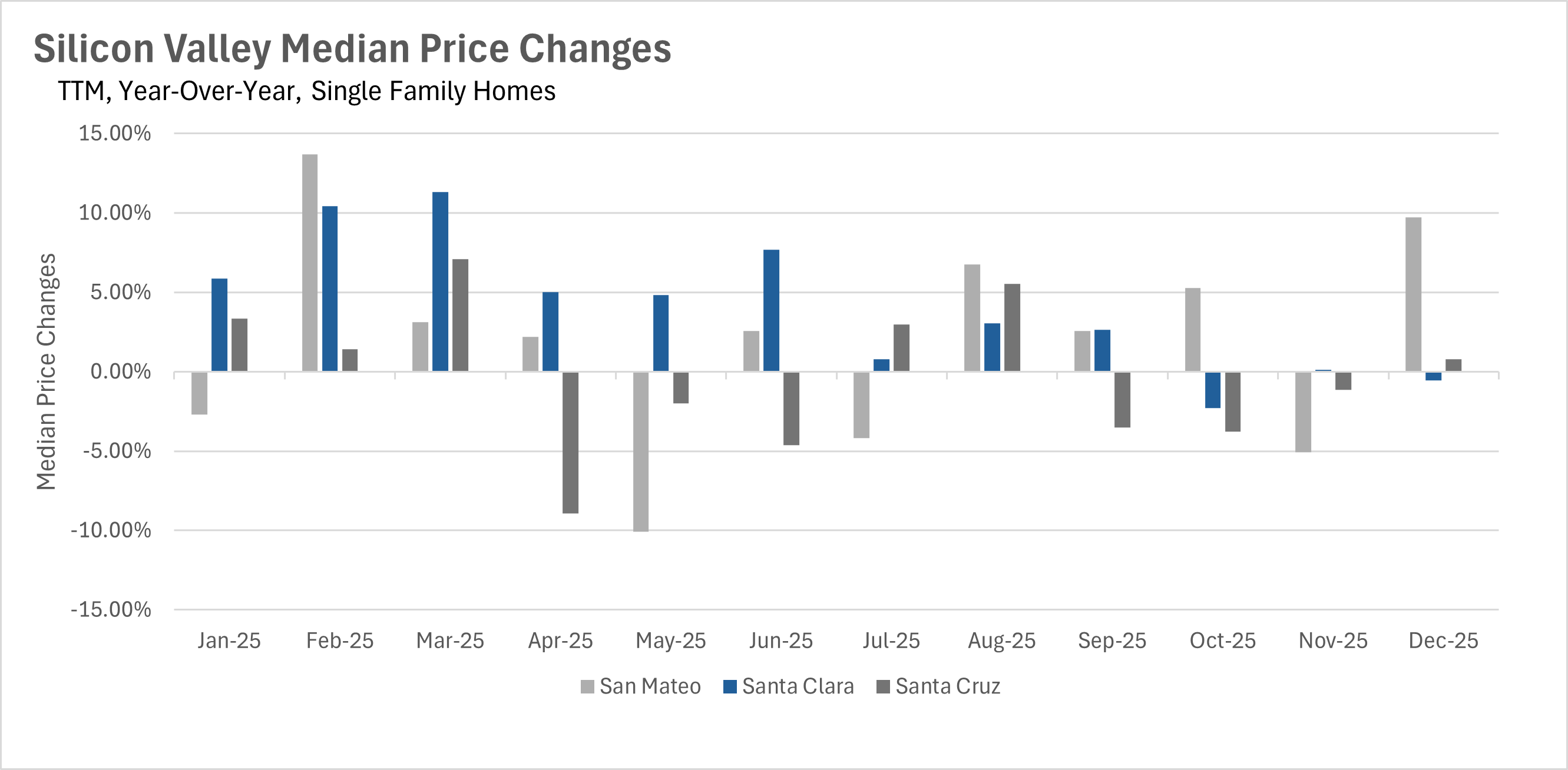

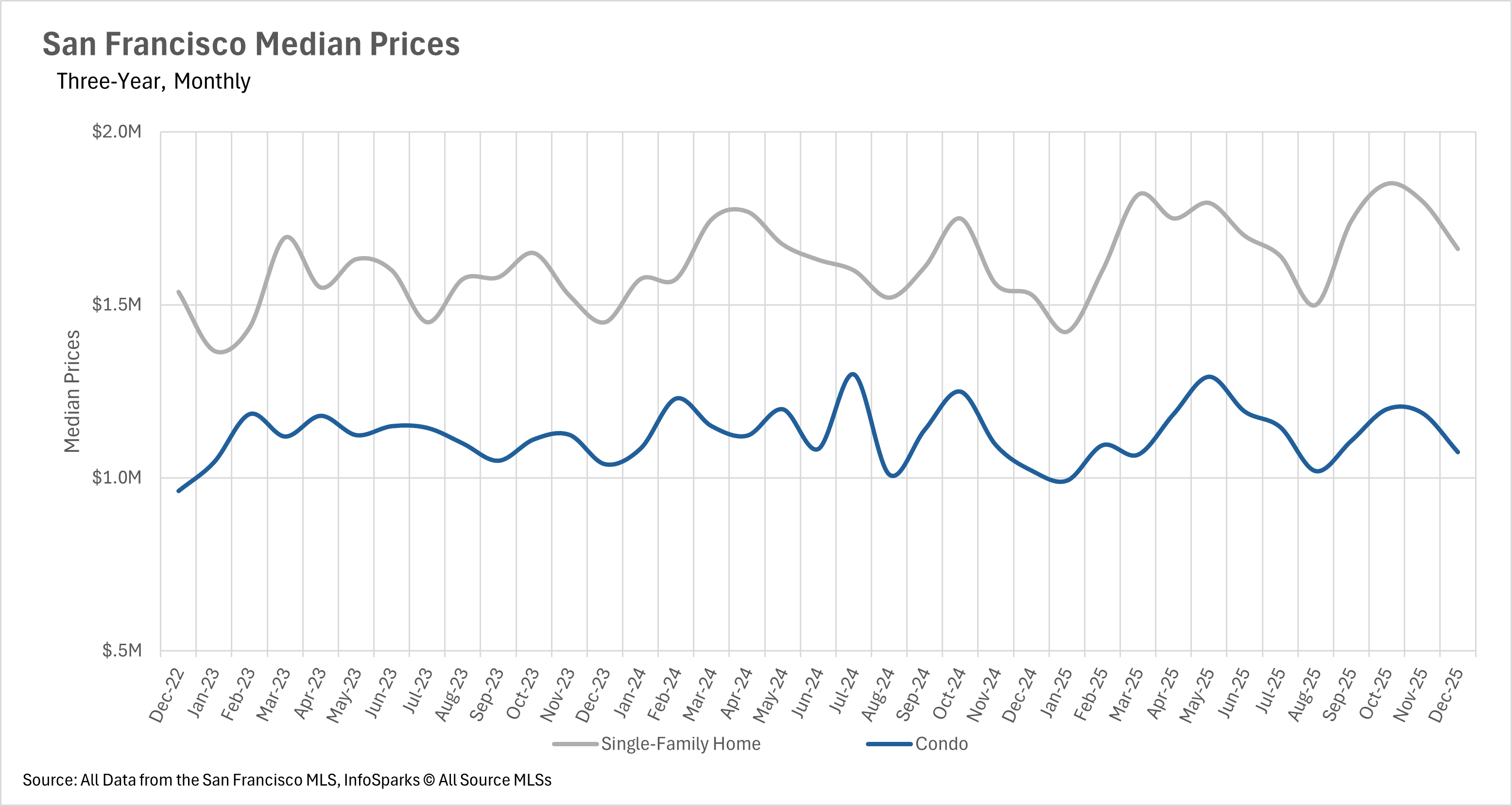

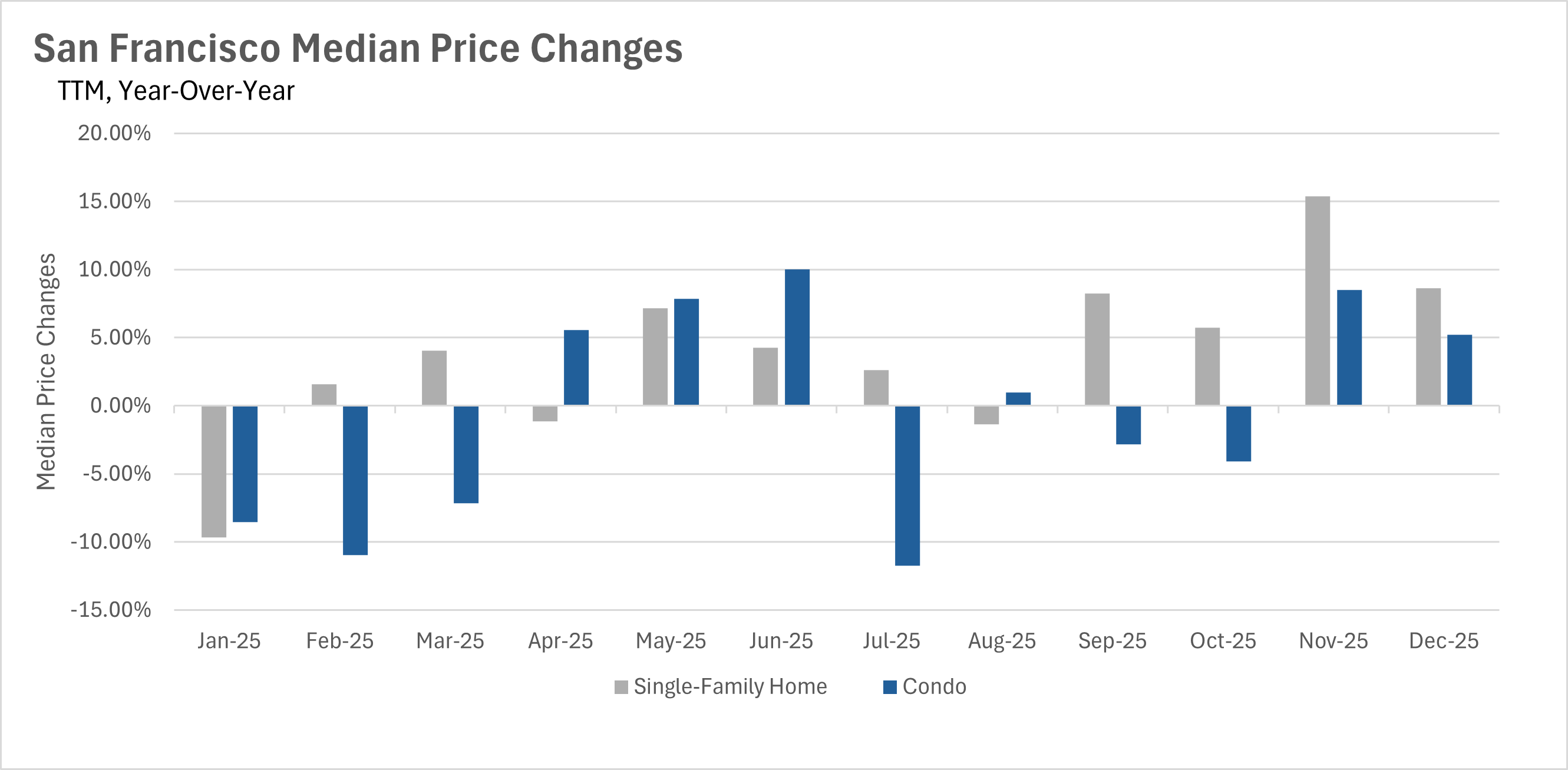

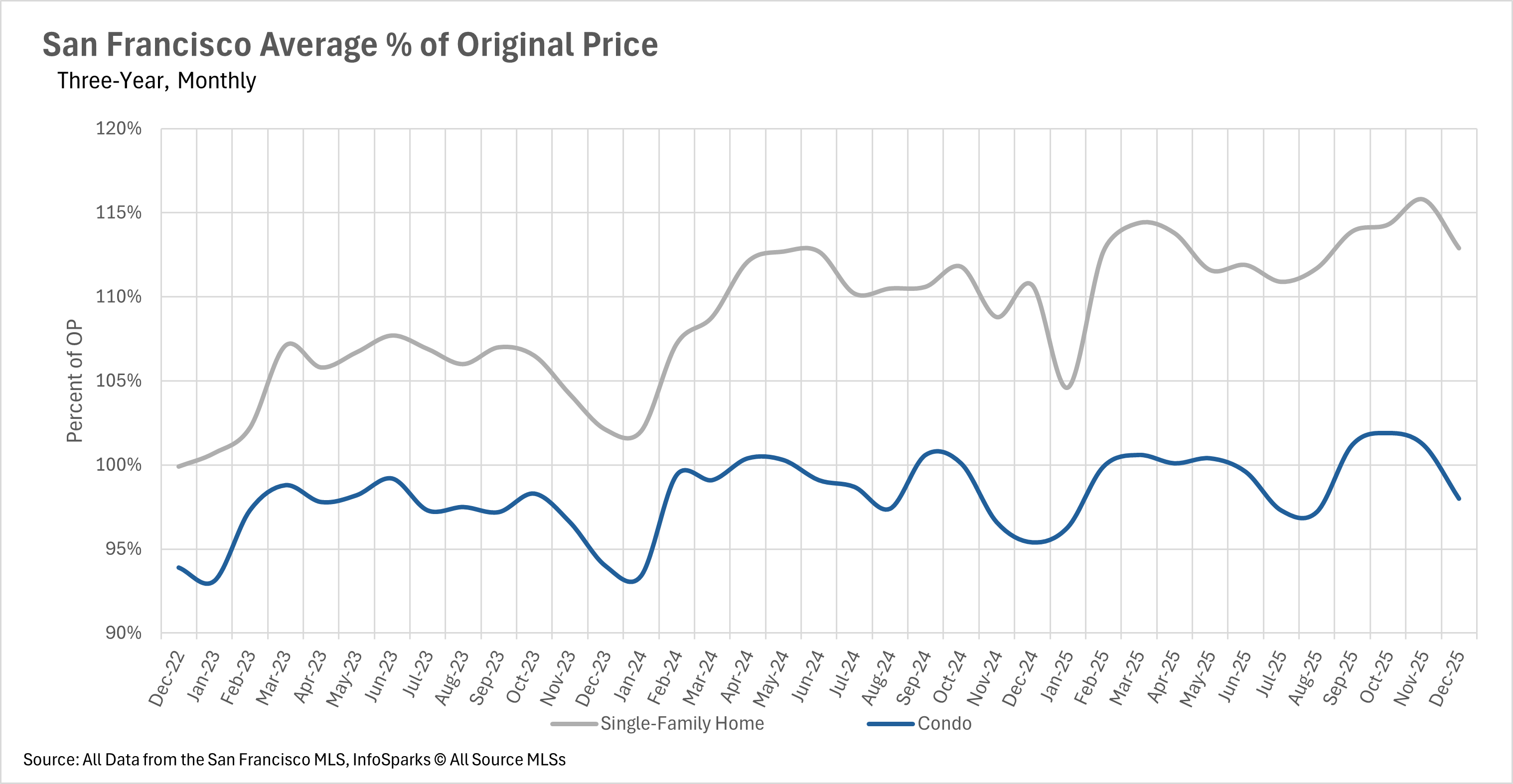

December brought mixed price performance across the Bay Area, with San Francisco leading appreciation while other regions showed varying results. San Francisco ended 2025 on a high note with single-family homes gaining 8.63% year-over-year to reach a median of $1,662,000, while condos rose 5.21% to $1,075,000. Single-family homes continue commanding significant premiums, selling for nearly 13% over asking price. Silicon Valley experienced a December rebound after November's rare across-the-board declines, with San Mateo County leading at 9.74% year-over-year gains to $1,887,500, while Santa Clara County saw a modest 0.55% decline to $1,800,000 and Santa Cruz remained relatively stable with a 0.79% increase to $1,270,000. Silicon Valley condos showed volatility, with San Mateo down 3.84%, Santa Clara up 1.71%, and Santa Cruz surging 10.48%.

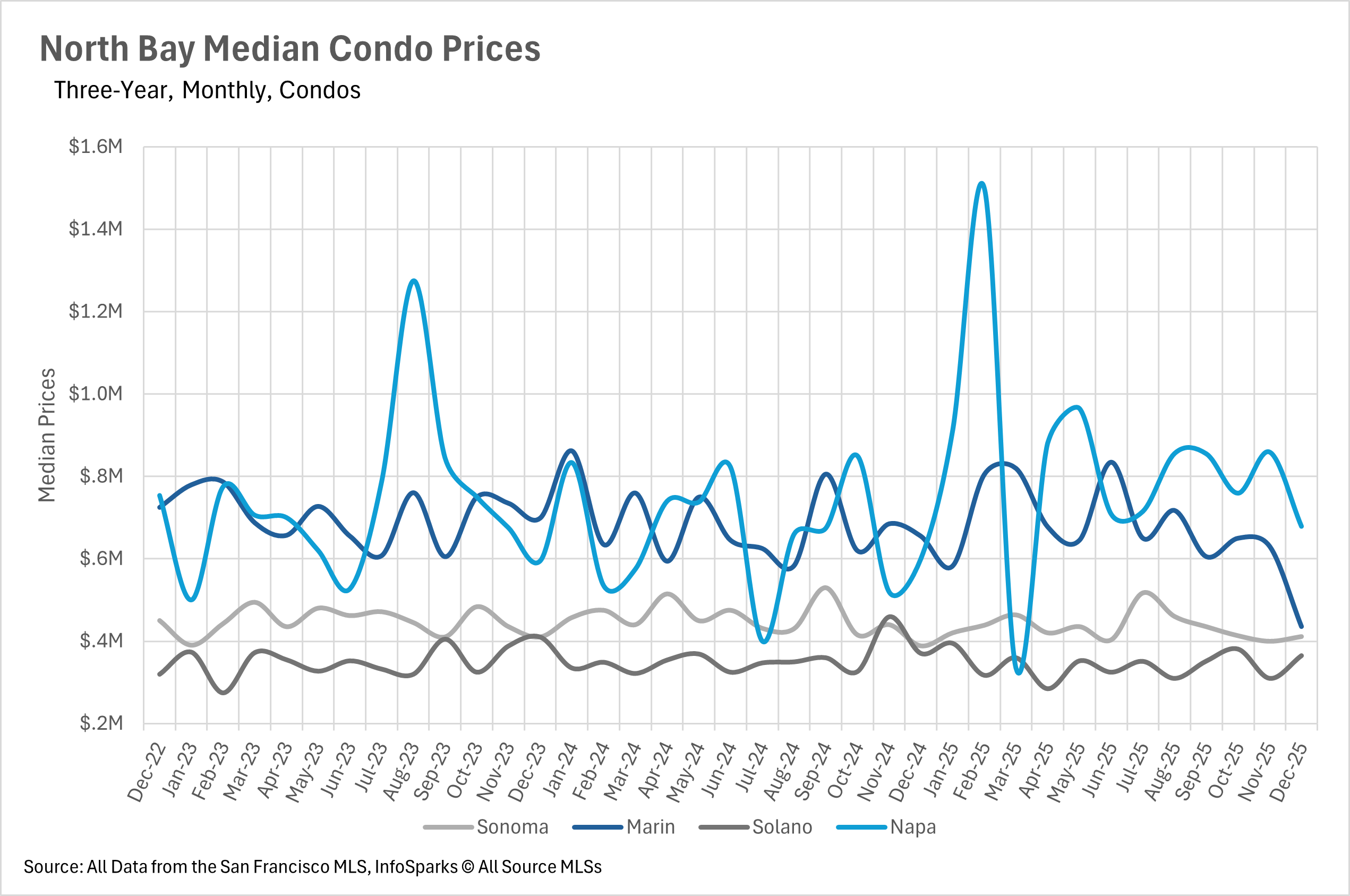

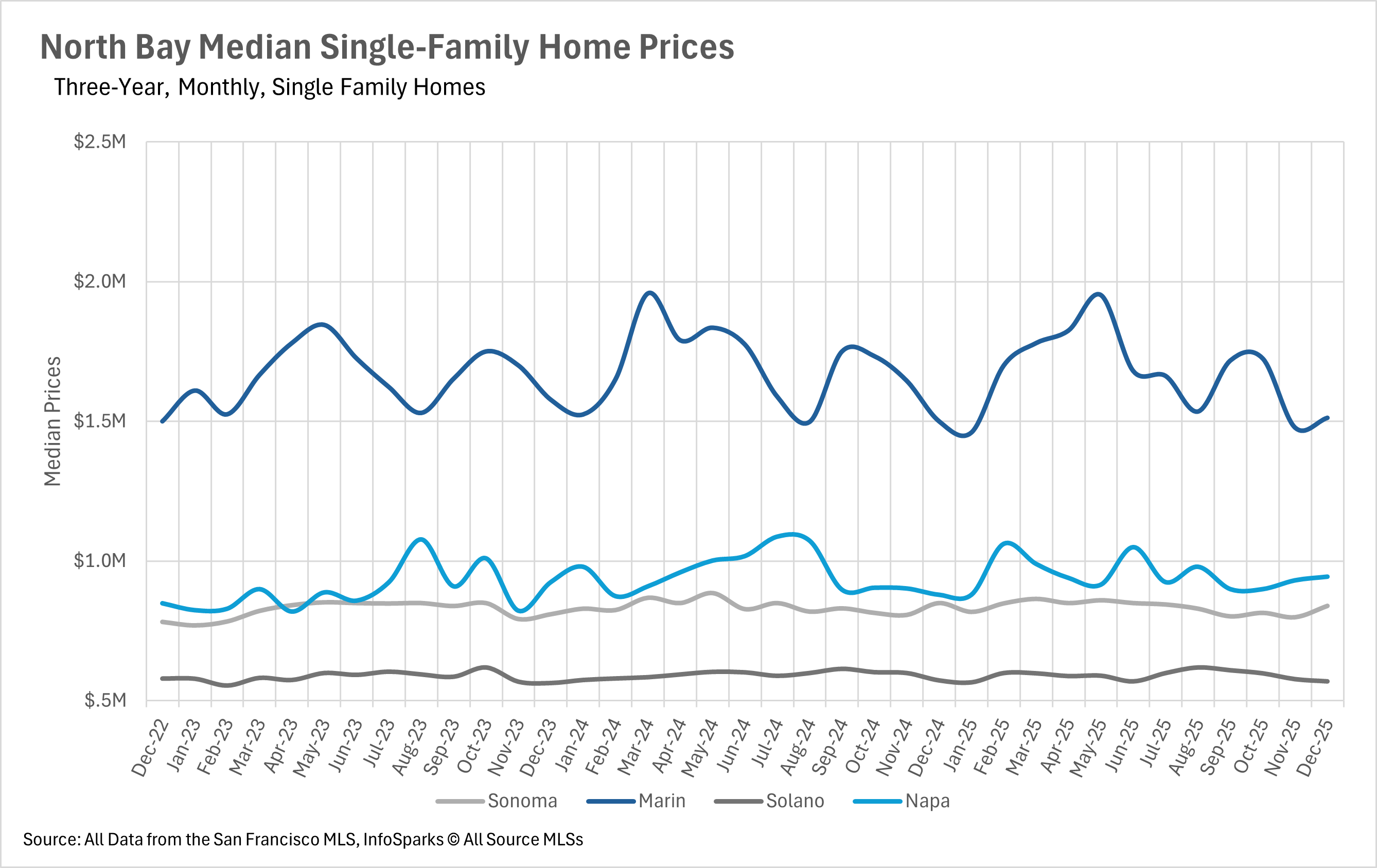

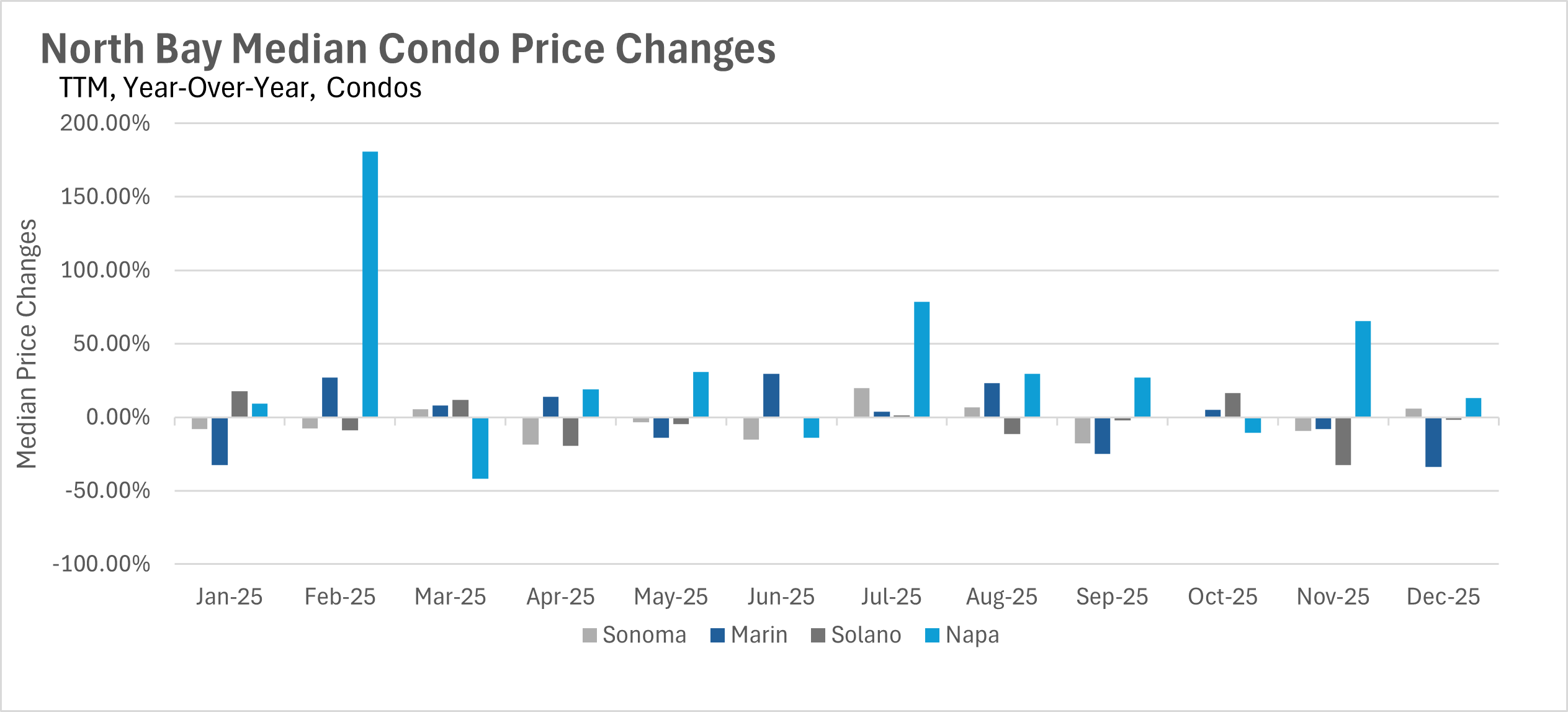

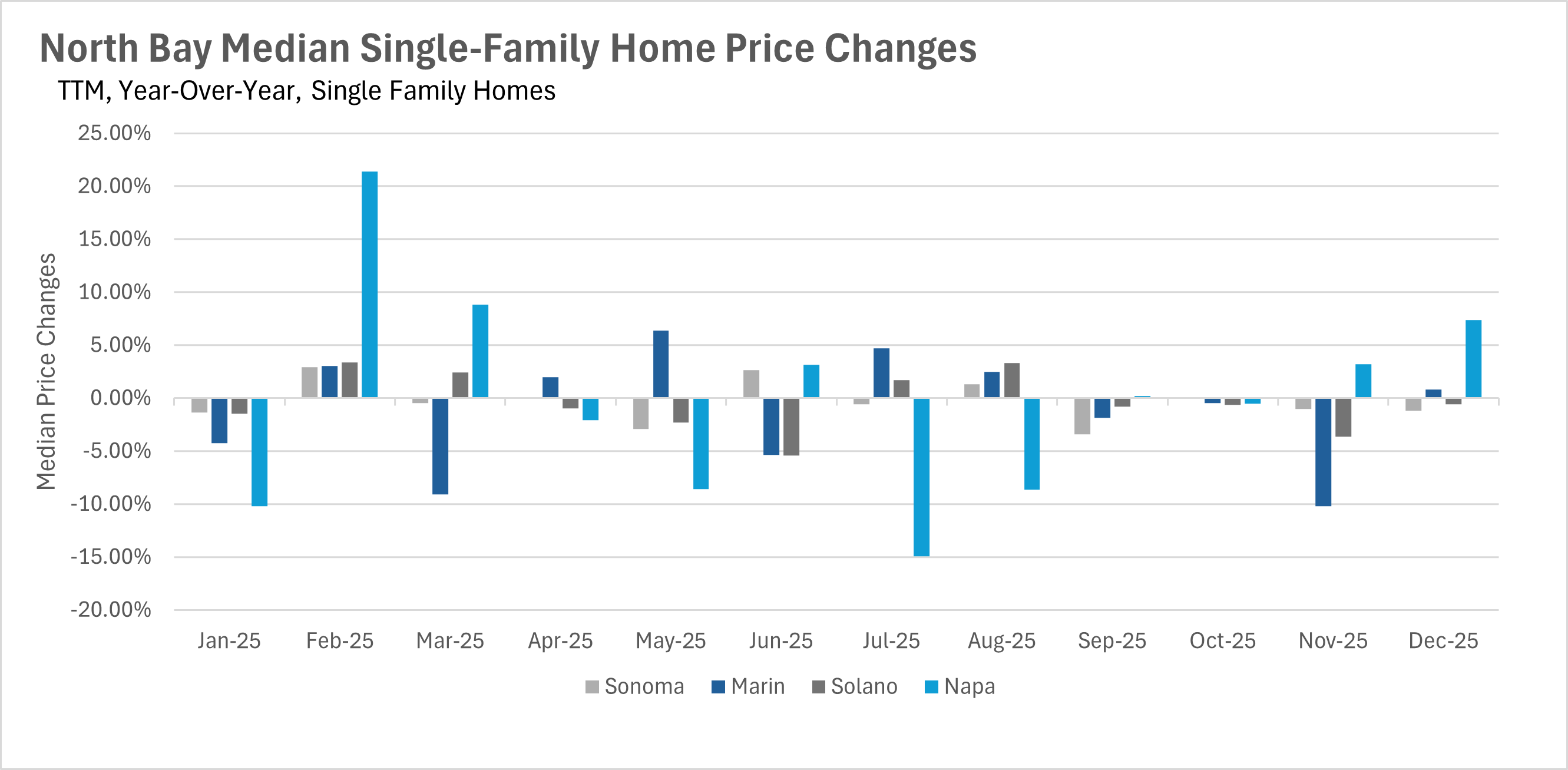

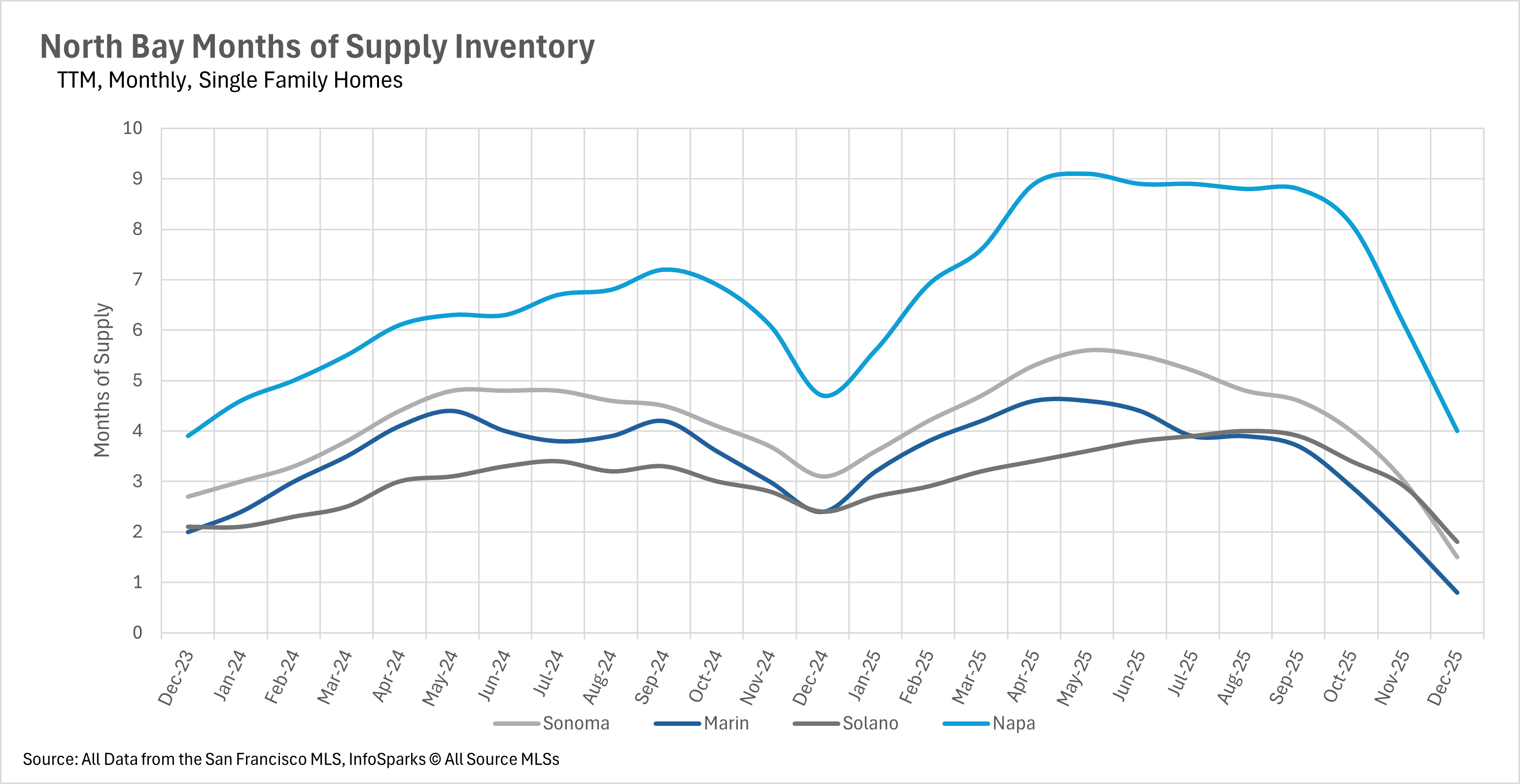

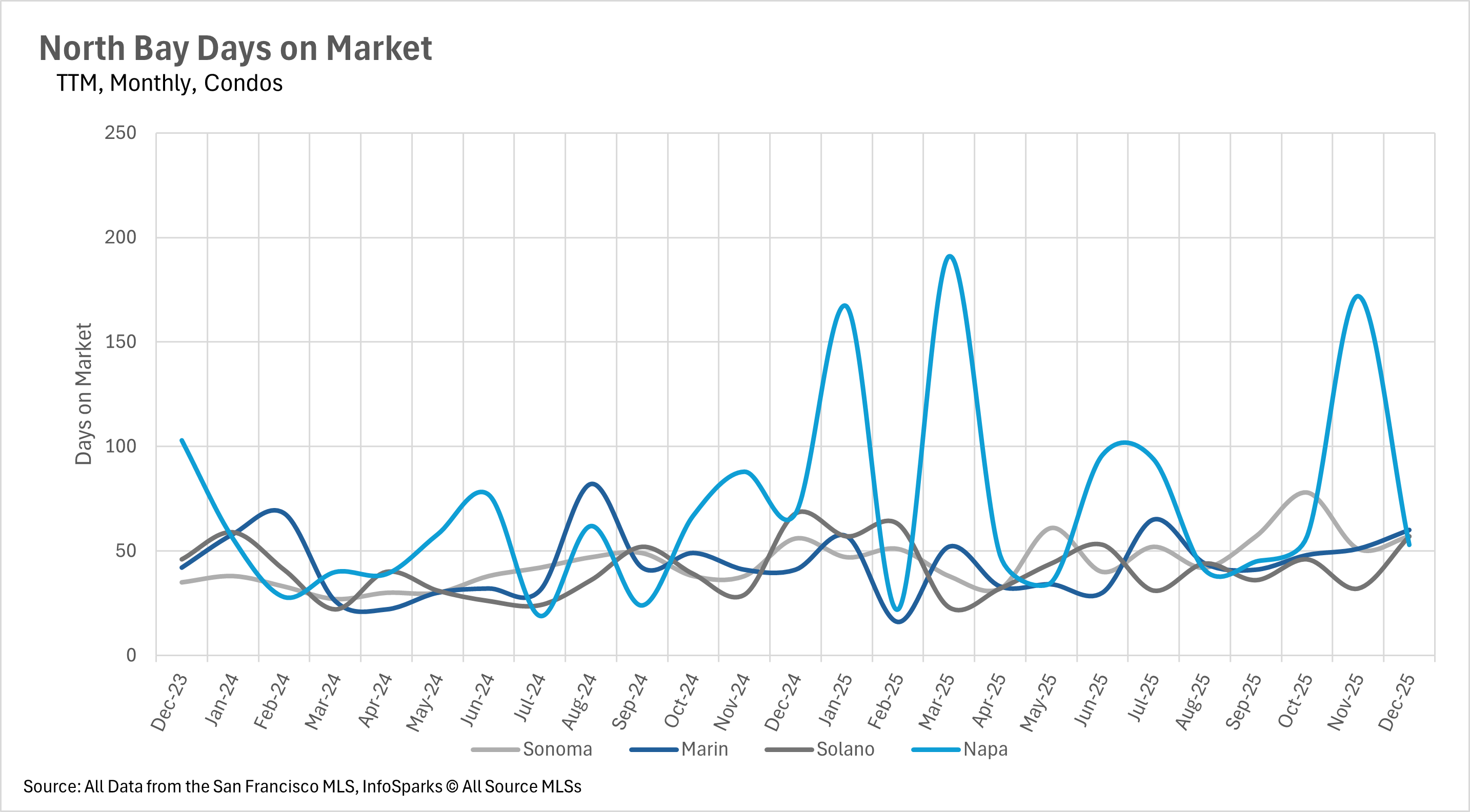

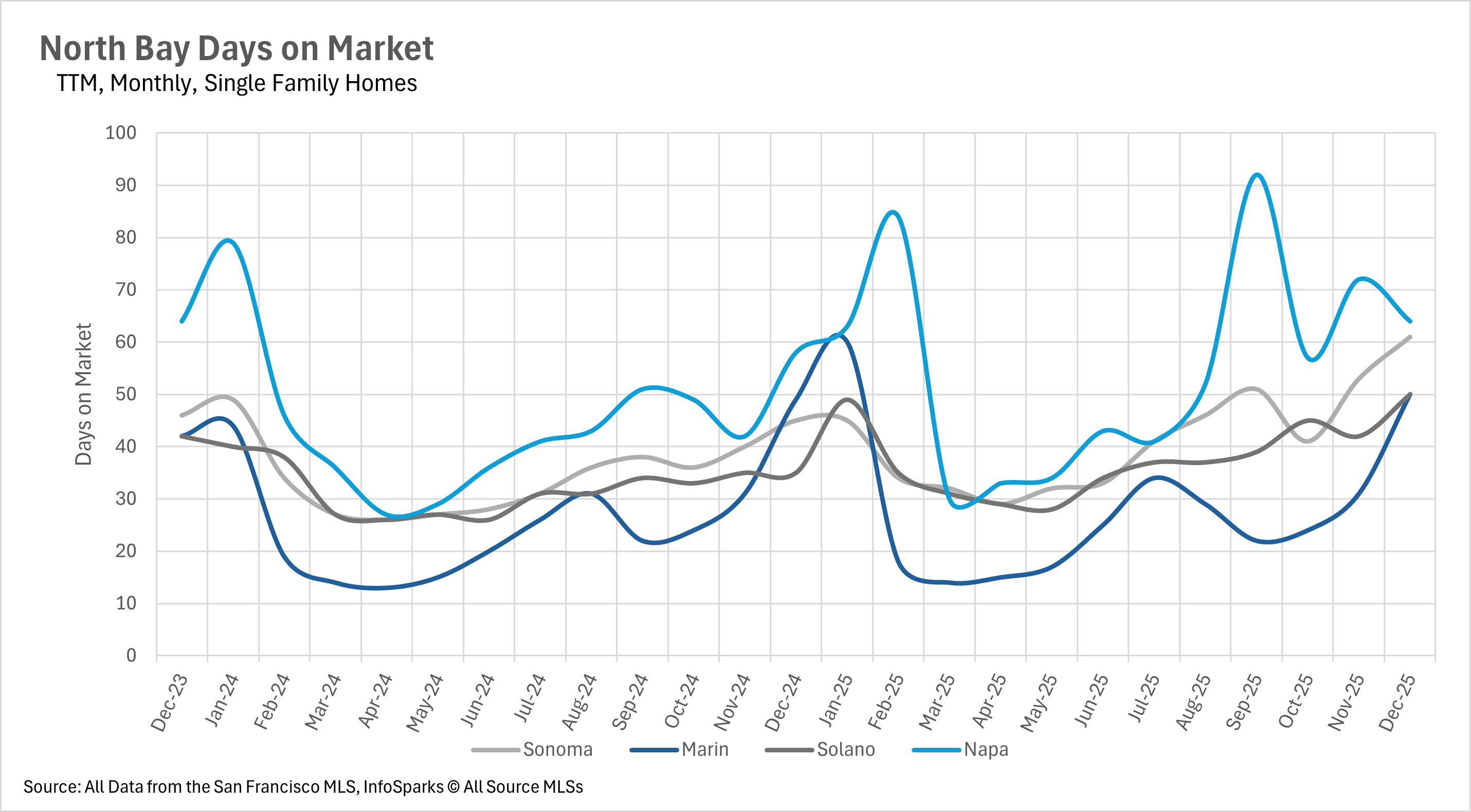

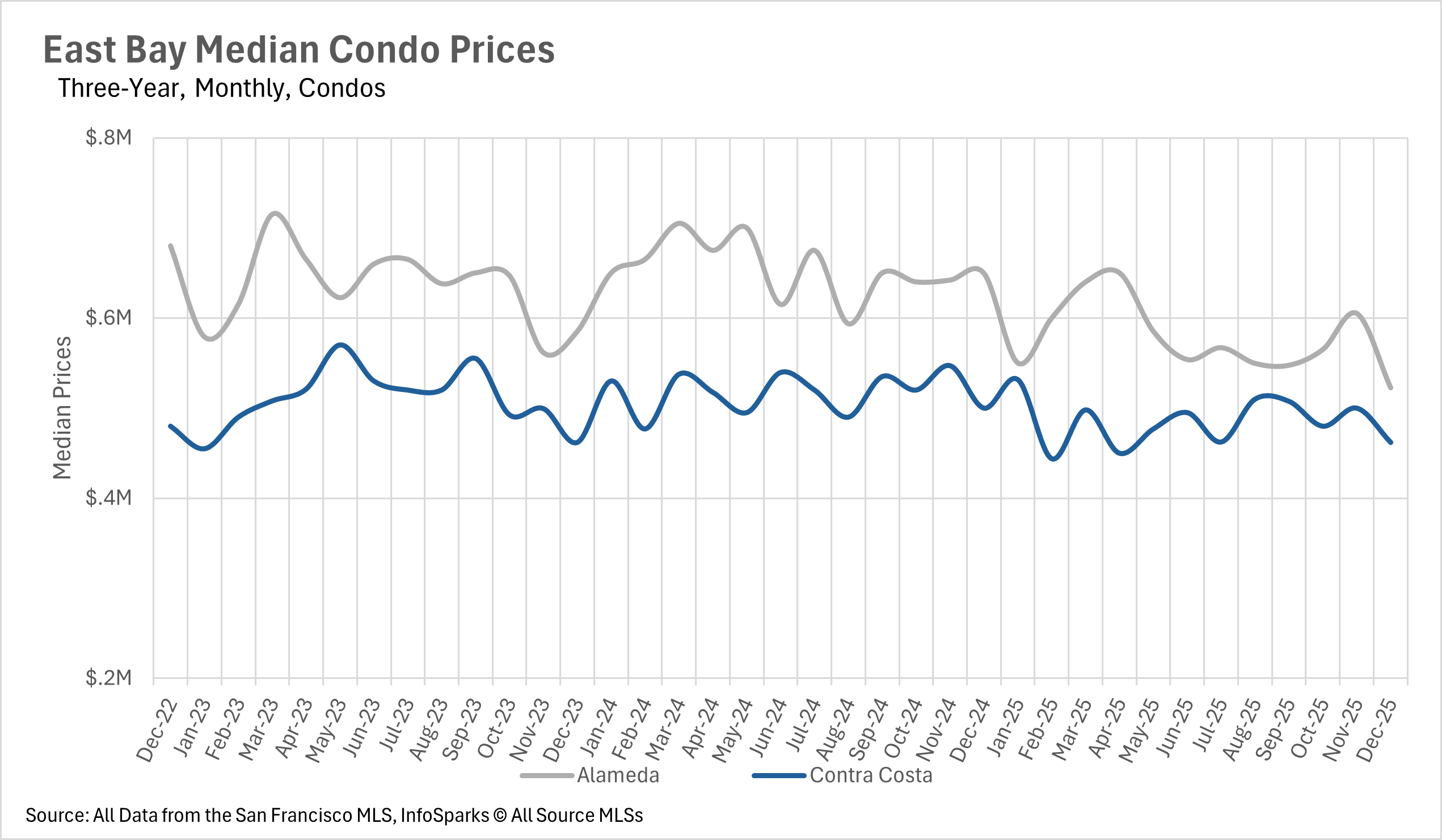

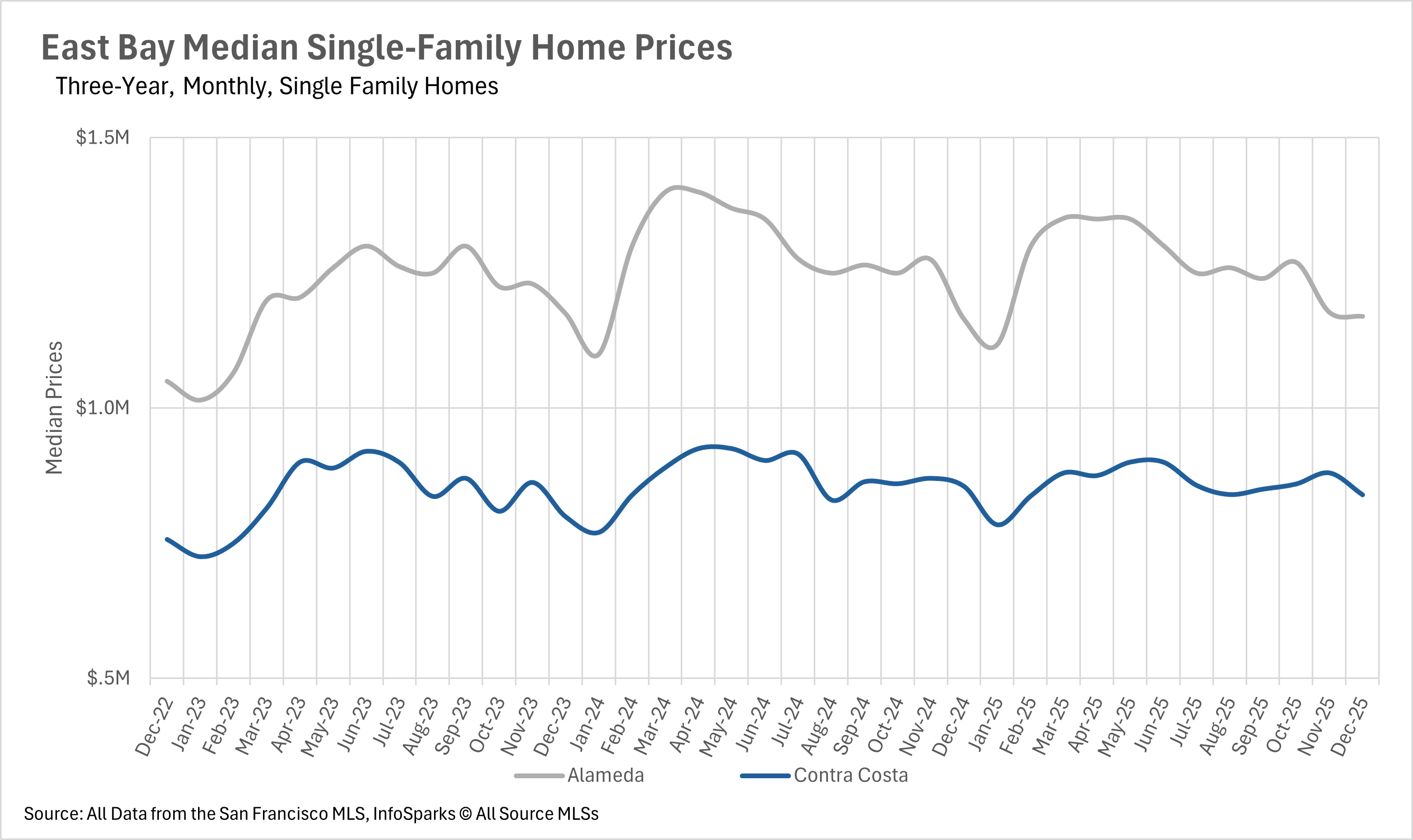

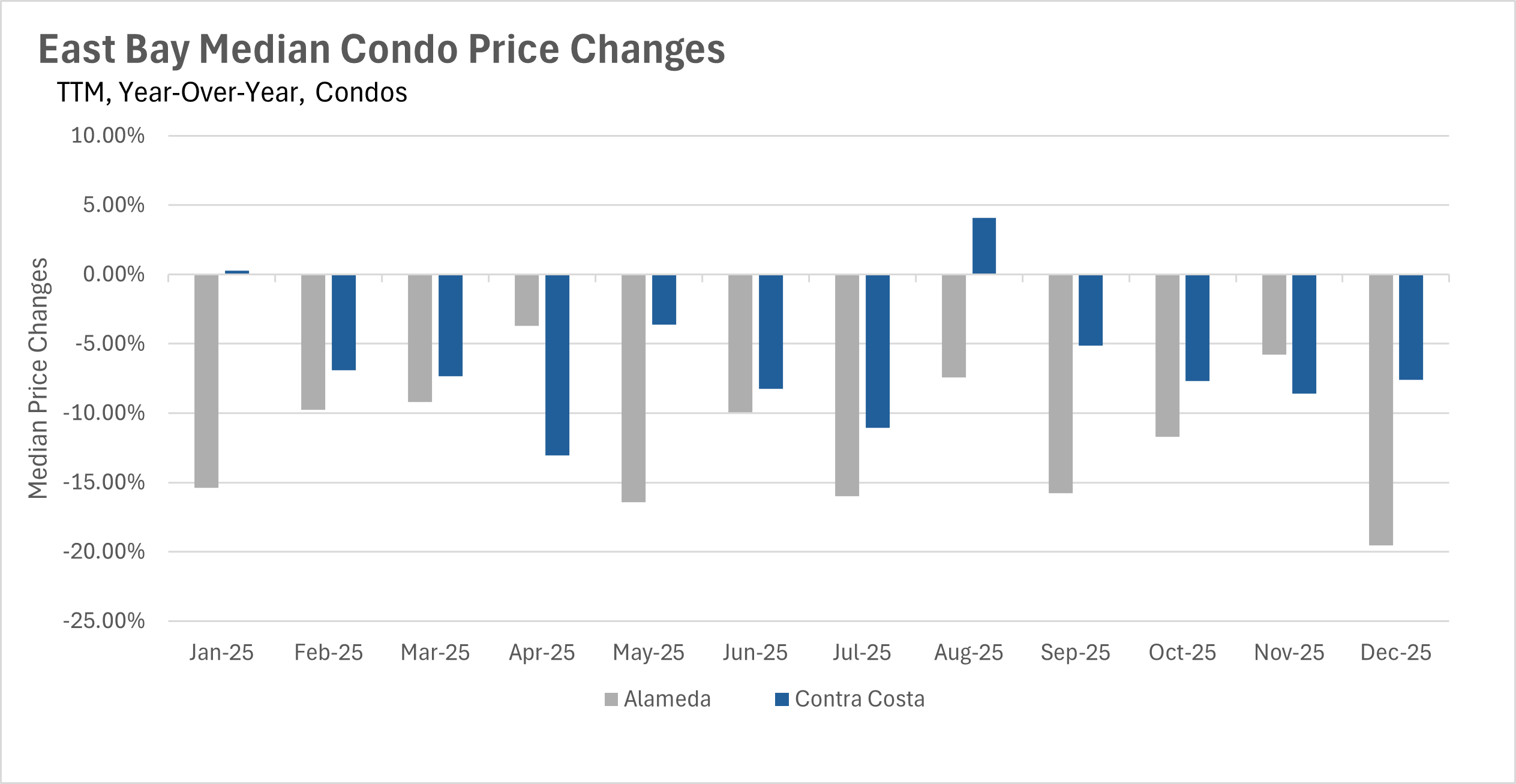

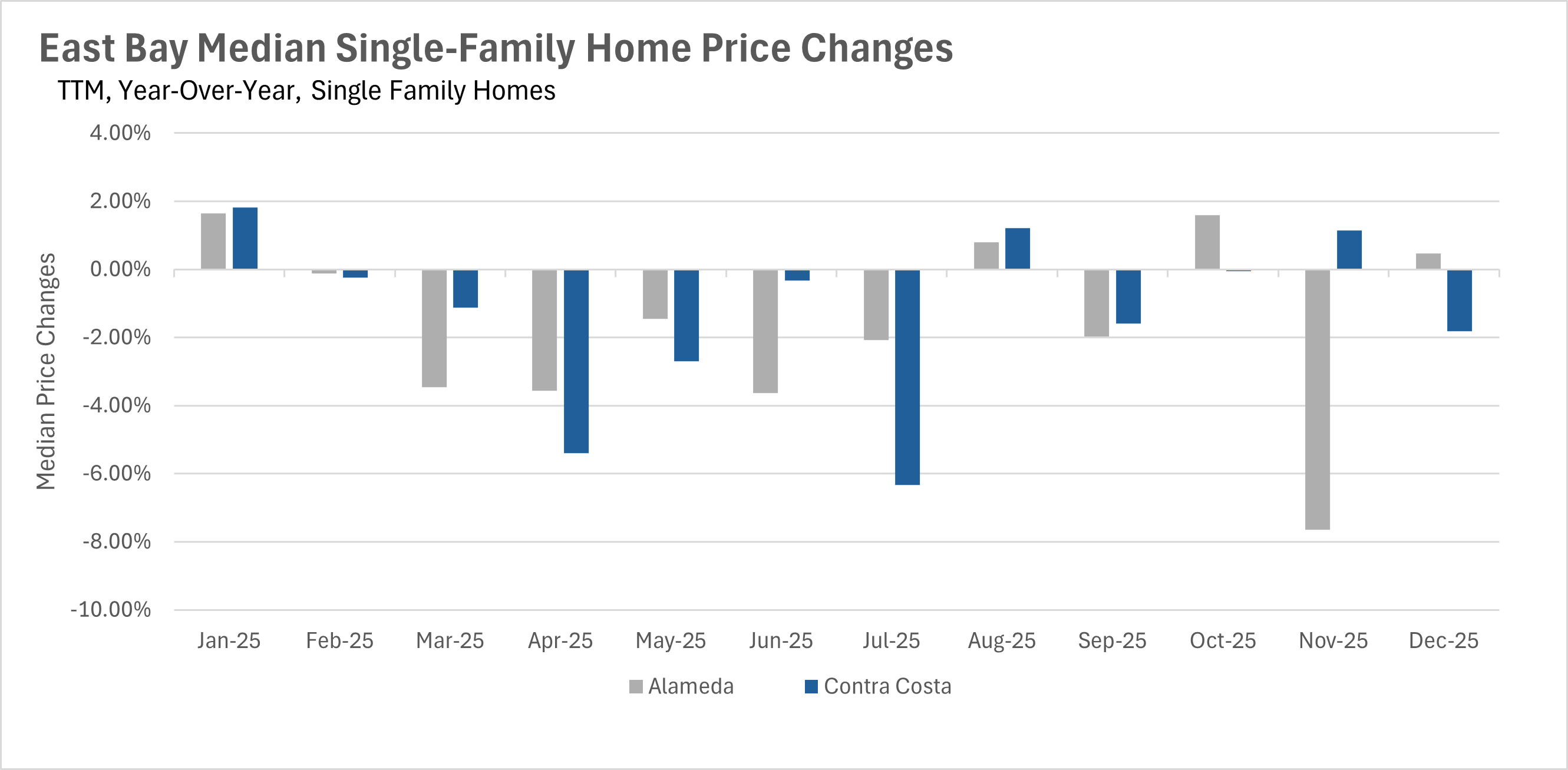

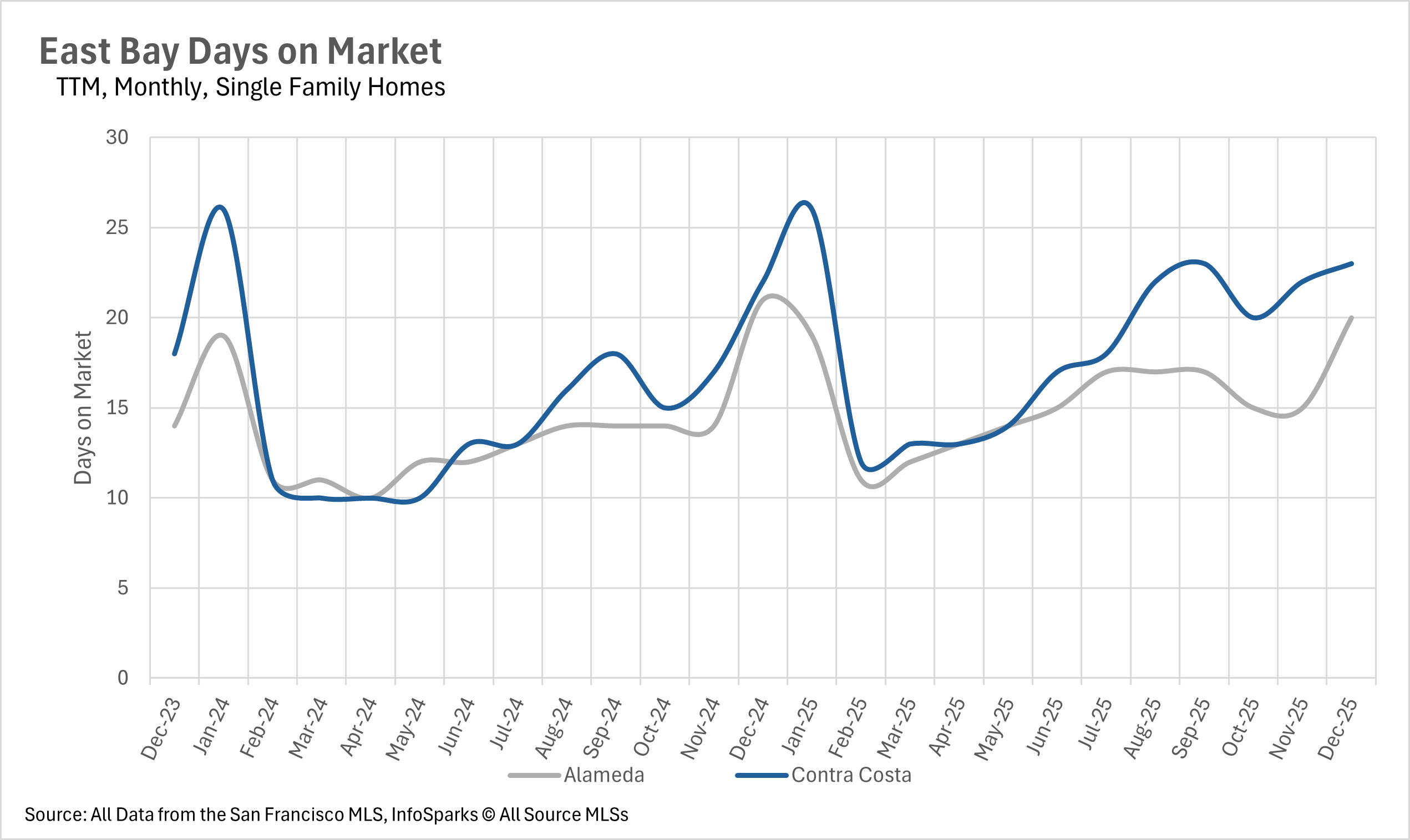

The East Bay demonstrated relative stability in single-family homes, with Alameda County up just 0.47% to $1,170,000 and Contra Costa down 1.81% to $839,500, though condos continued struggling with Alameda plummeting 19.55% to $522,500 and Contra Costa falling 7.60% to $462,000. The North Bay presented a tale of two markets, with Napa County emerging as the clear winner at 7.34% growth to $944,624 and Marin up modestly 0.83% to $1,512,500, while Sonoma and Solano declined by 1.18% and 0.61% respectively. North Bay condos showed extreme volatility with Marin crashing 33.59% while Sonoma rose 5.86% and Napa gained 13.13%.

|

|

|