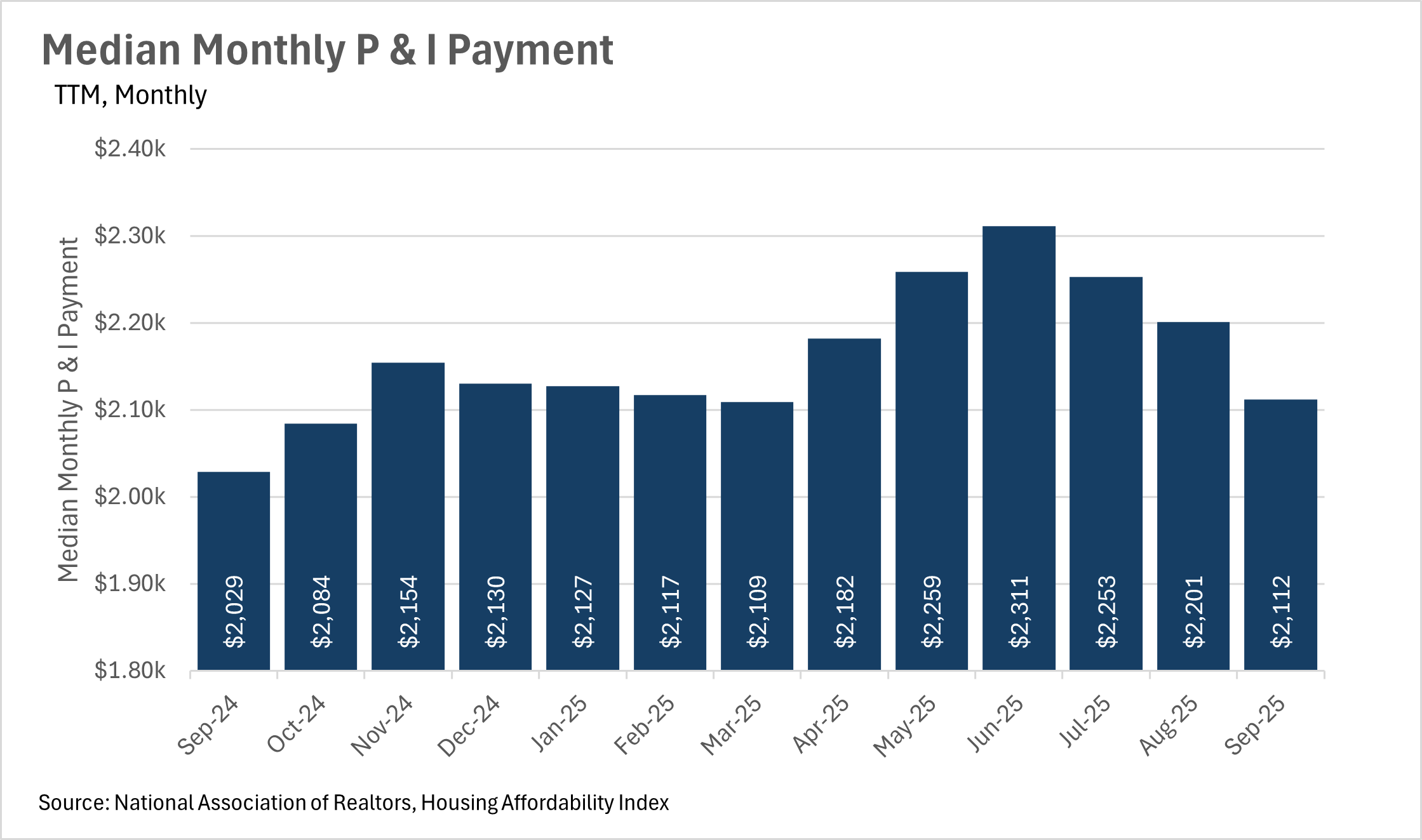

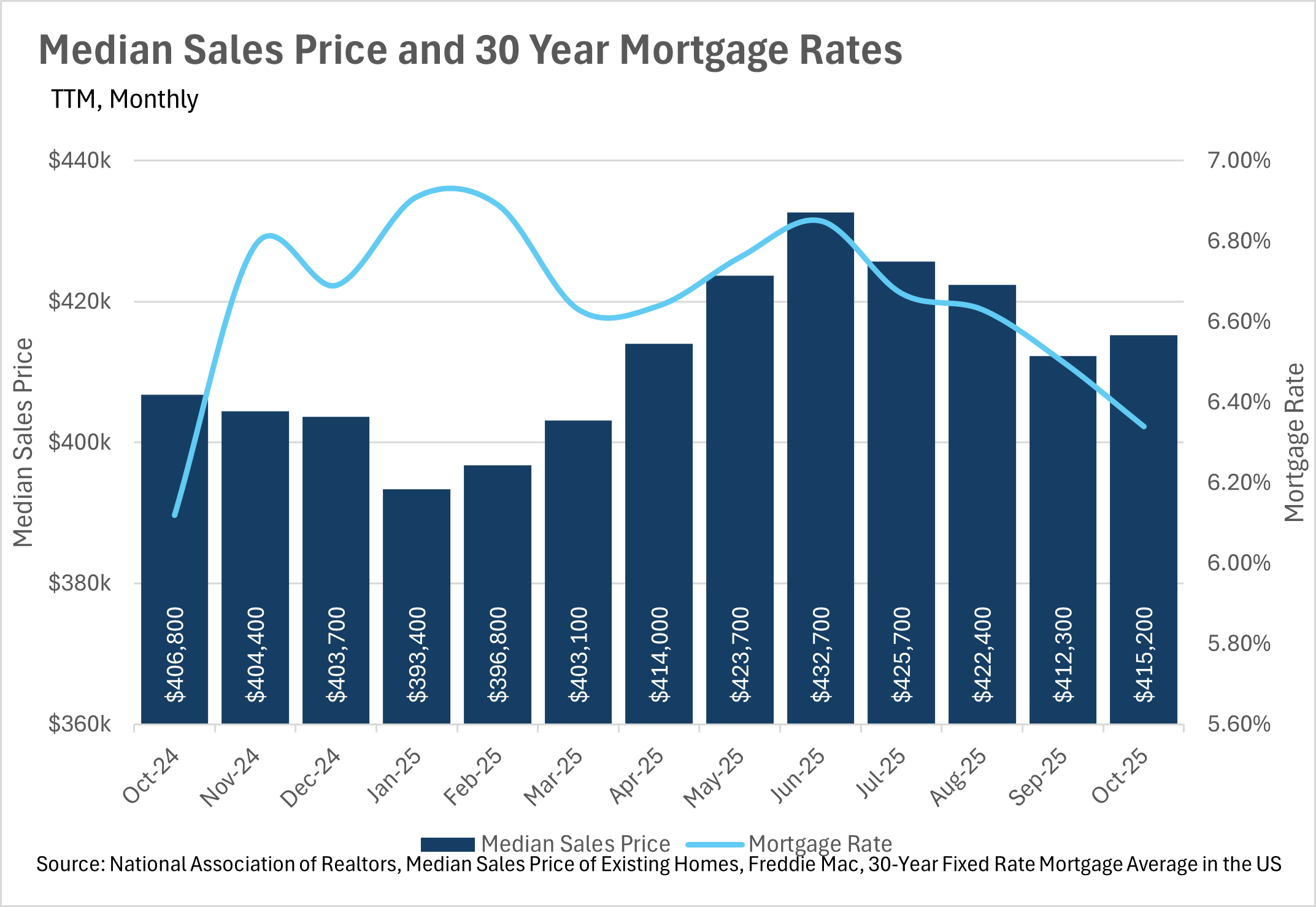

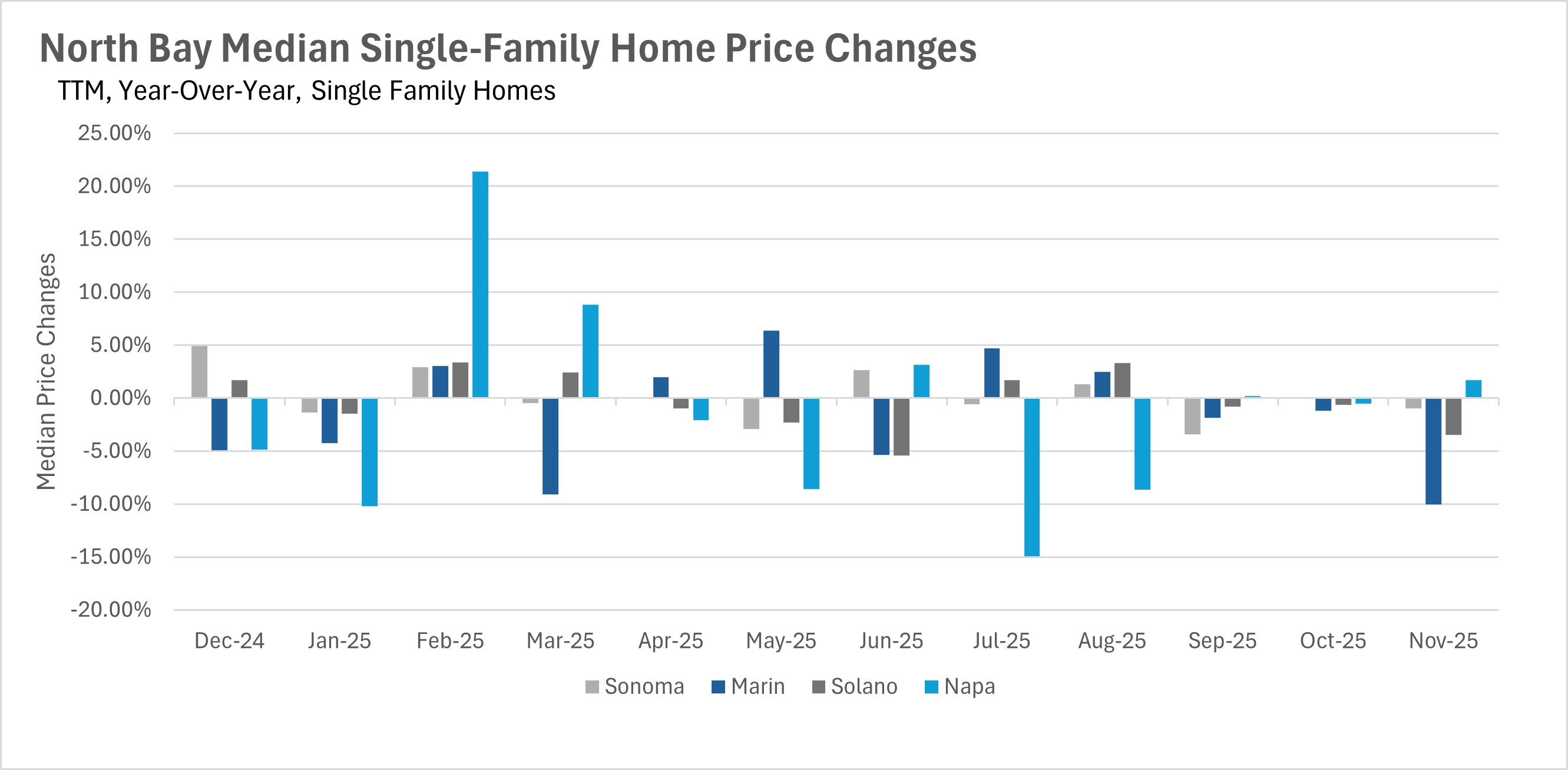

Although they are on the decline, interest rates remain much higher than the inflation rate...

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.