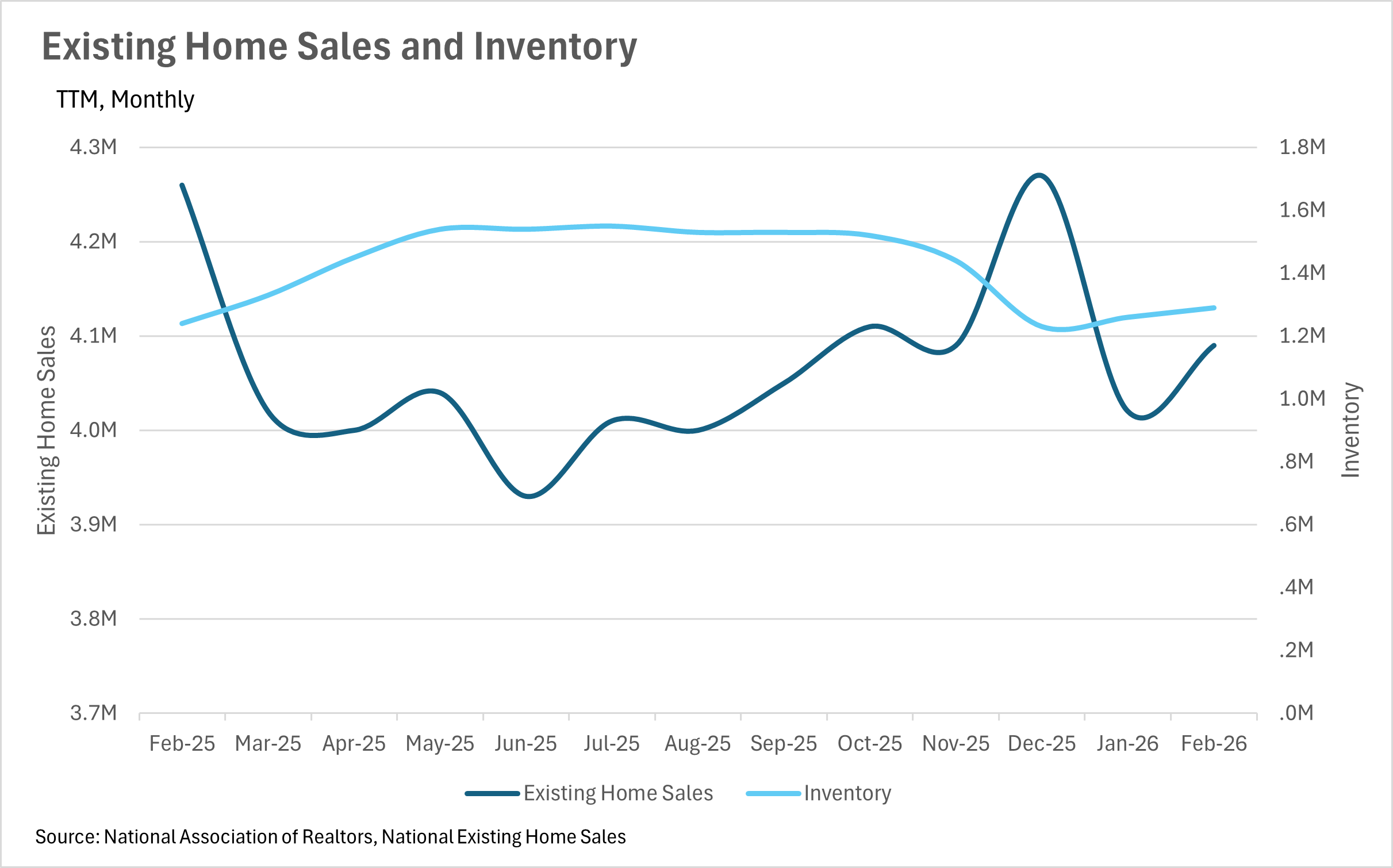

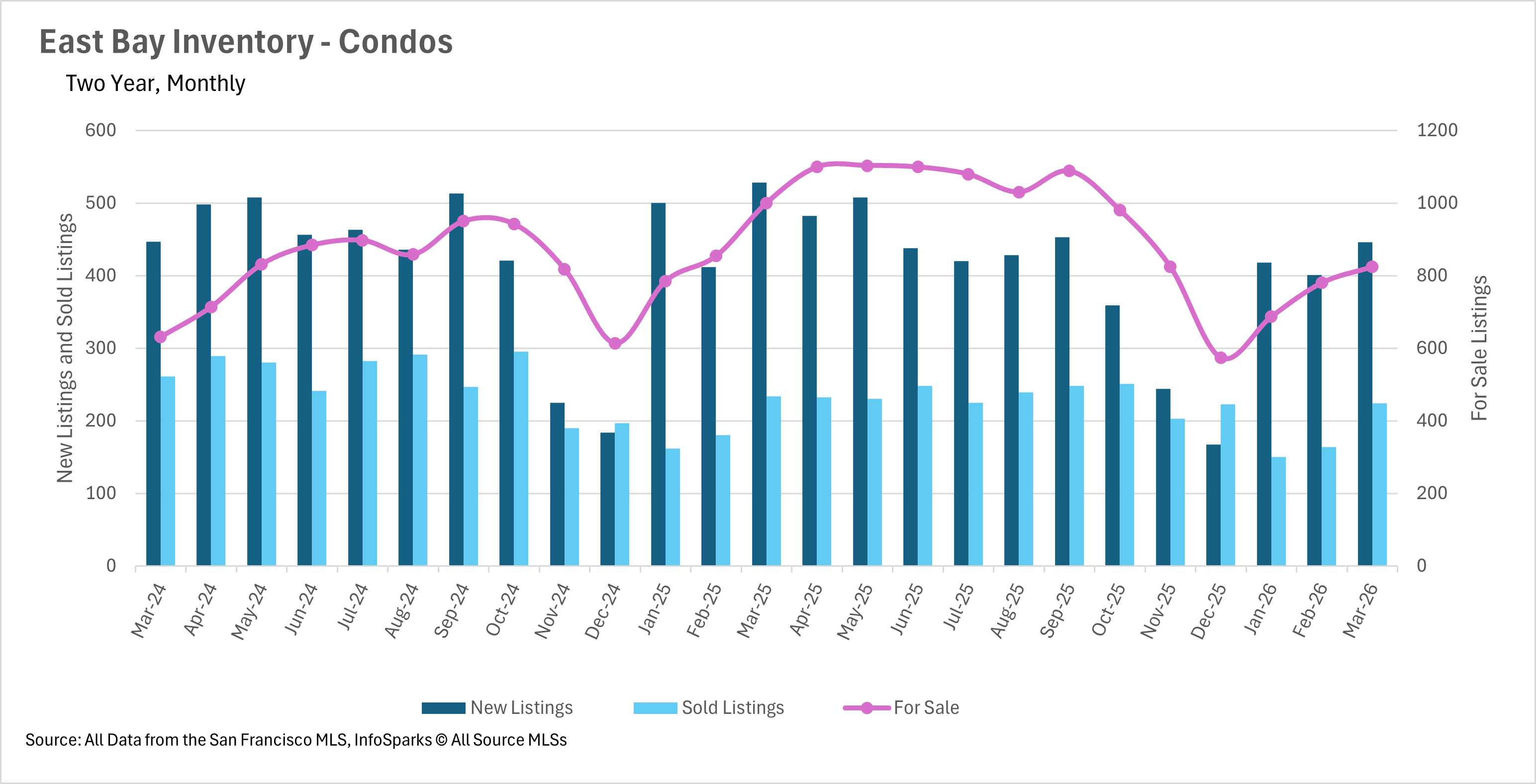

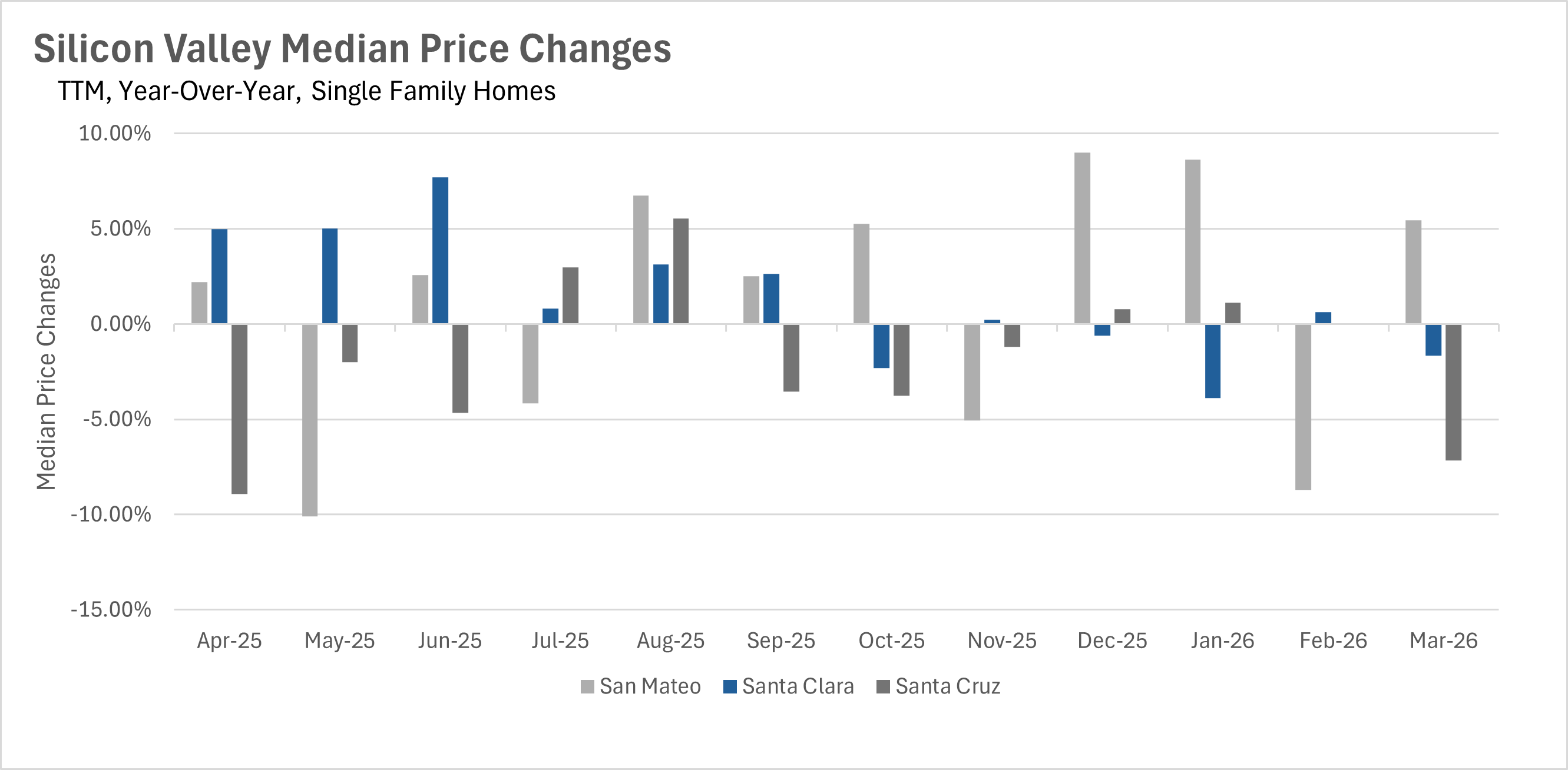

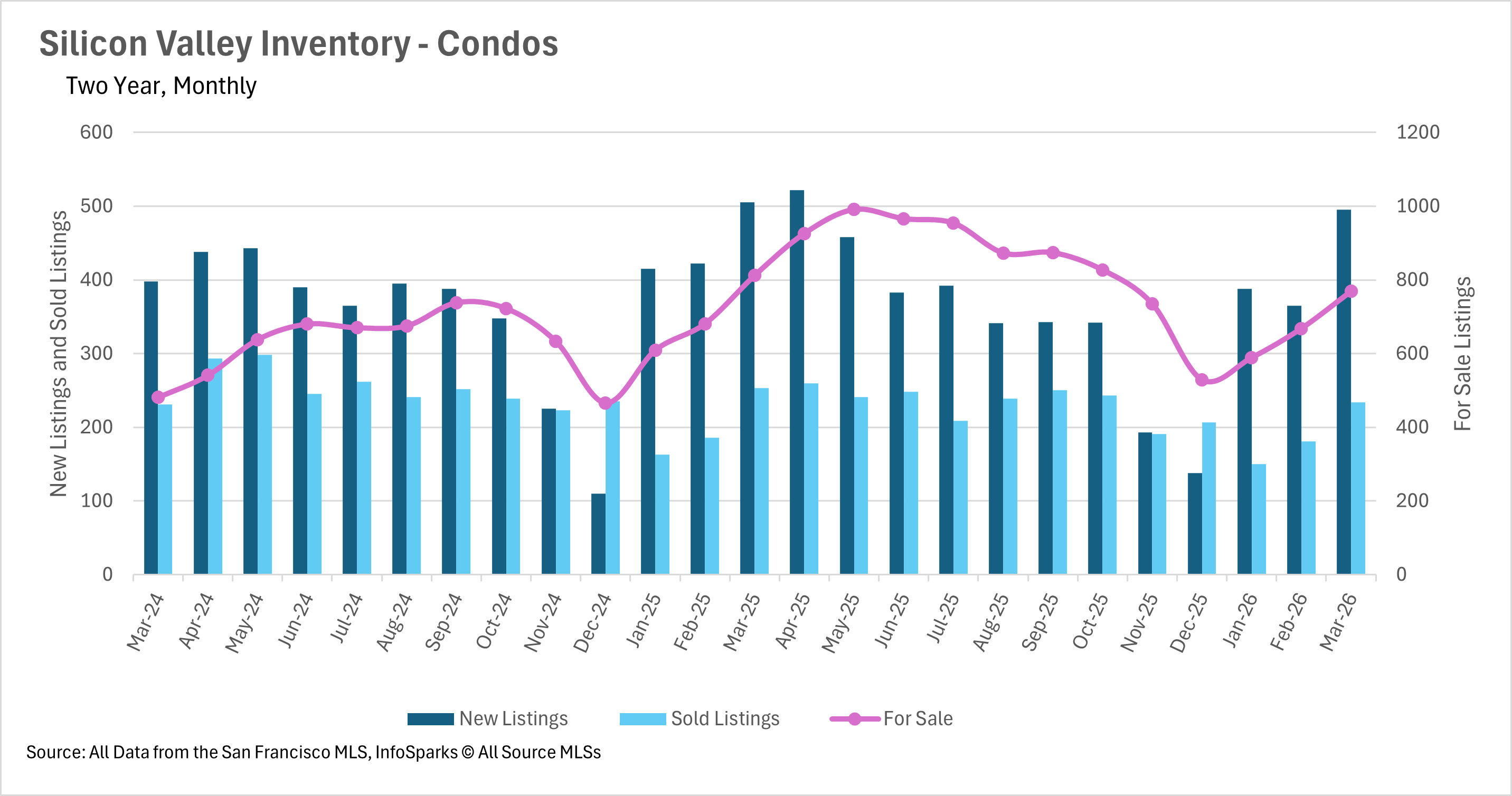

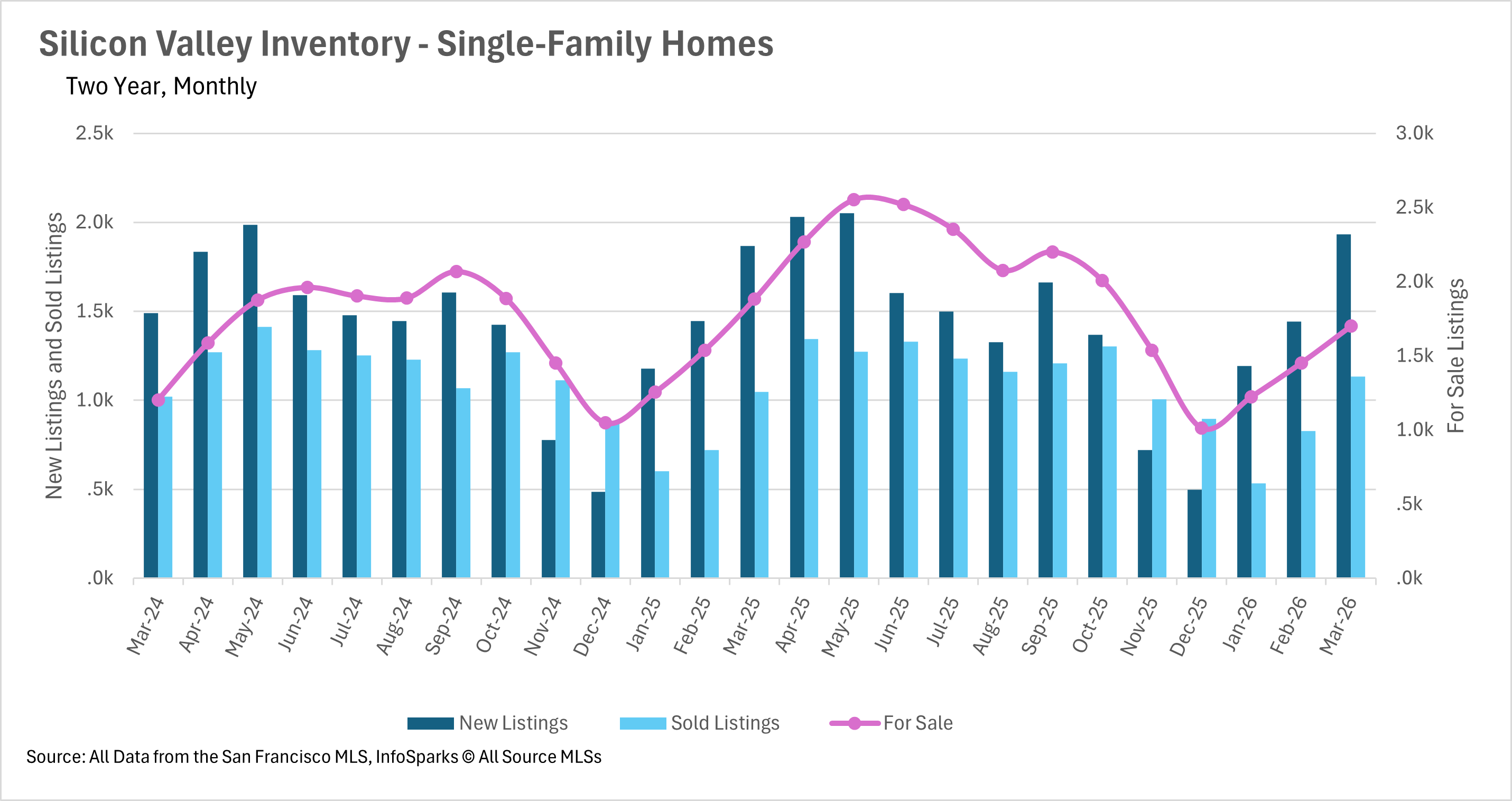

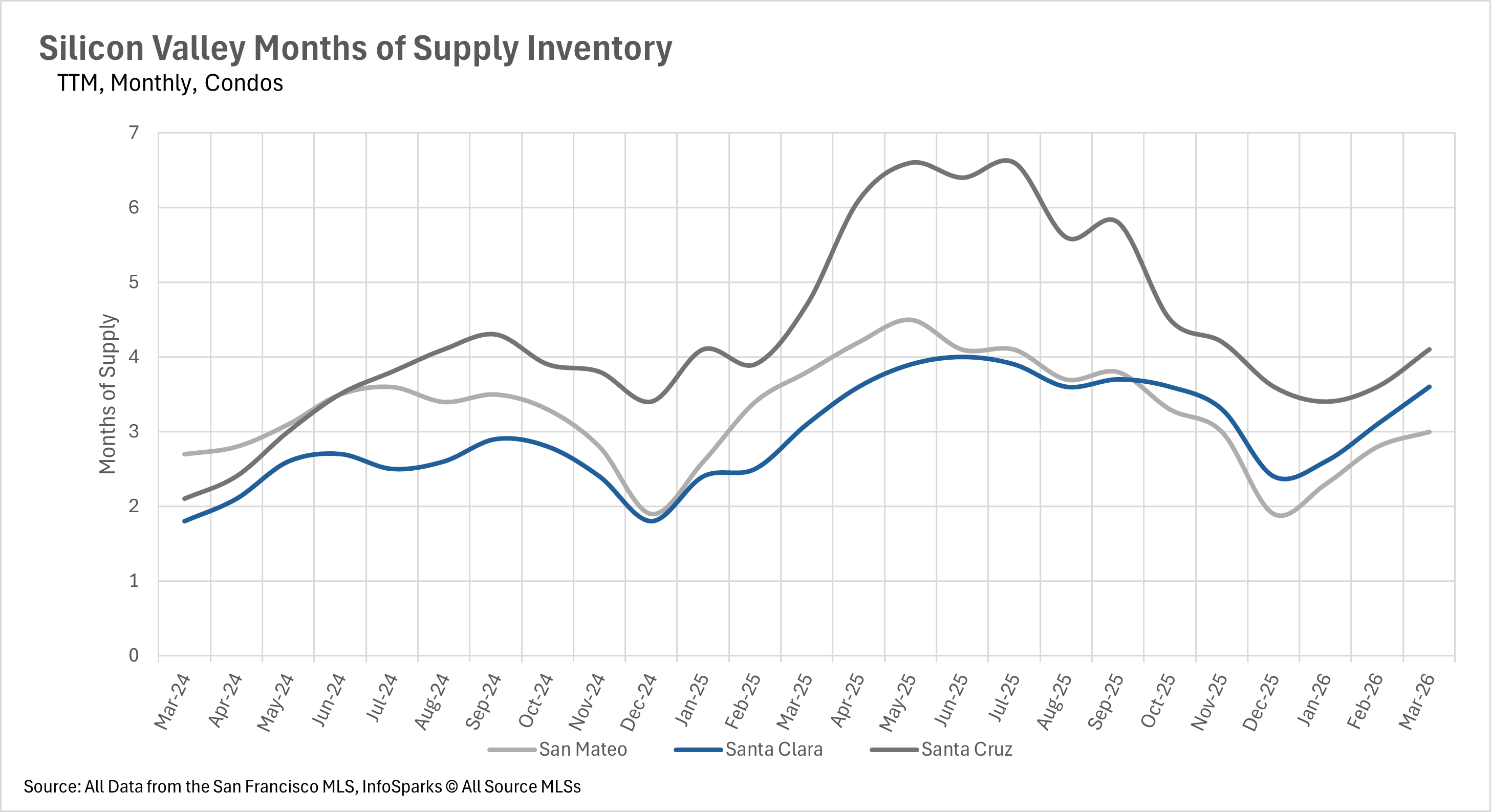

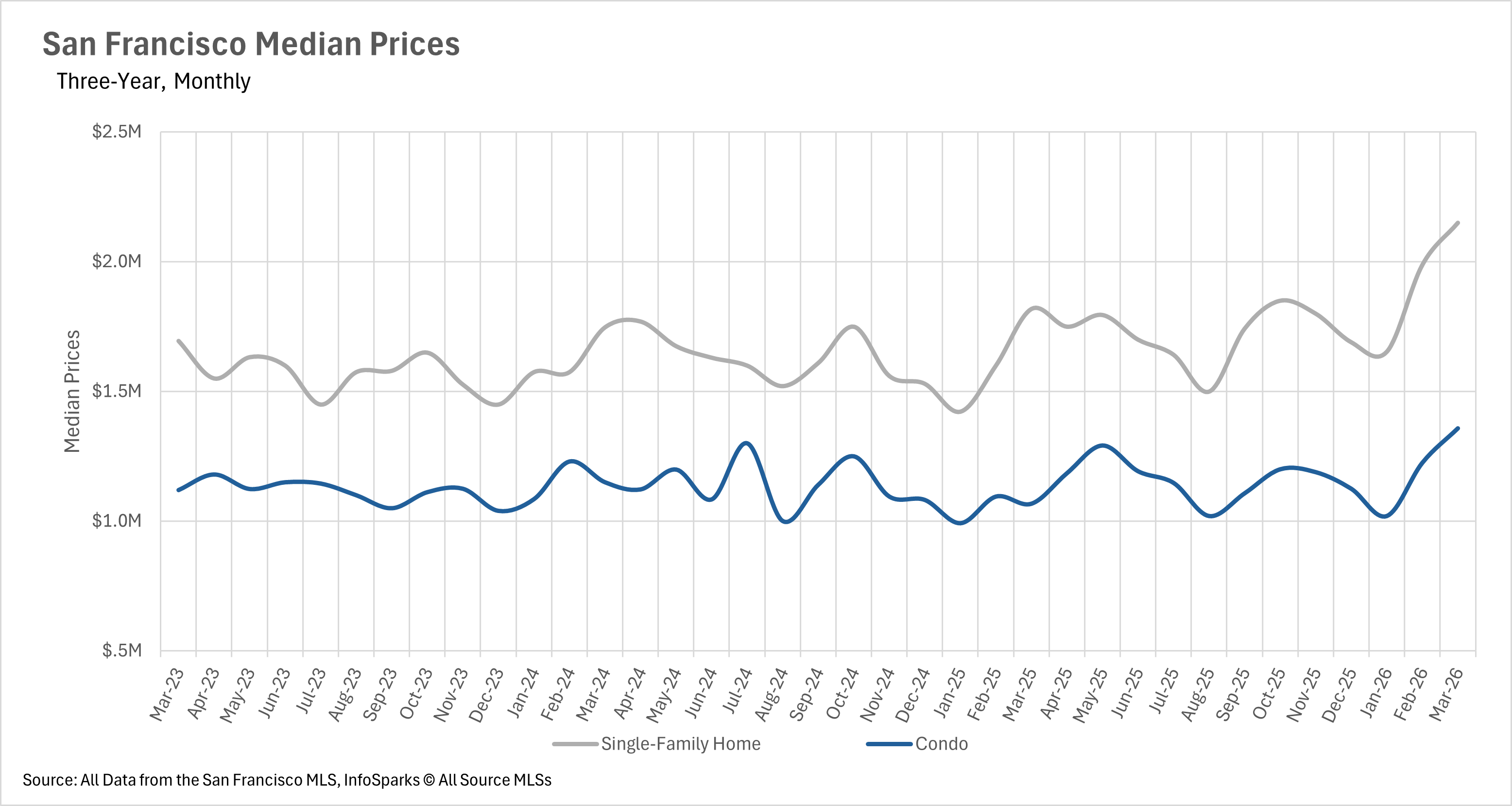

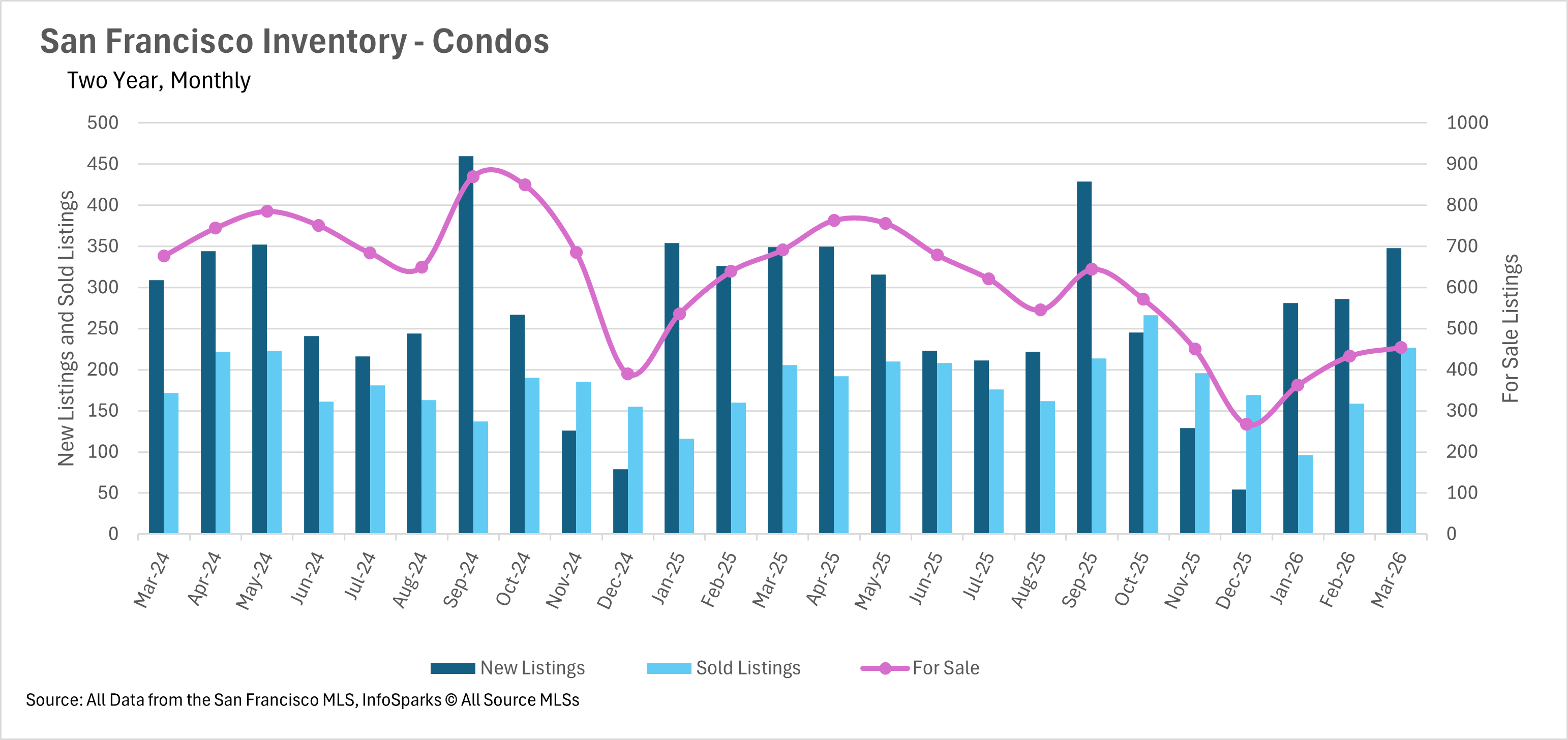

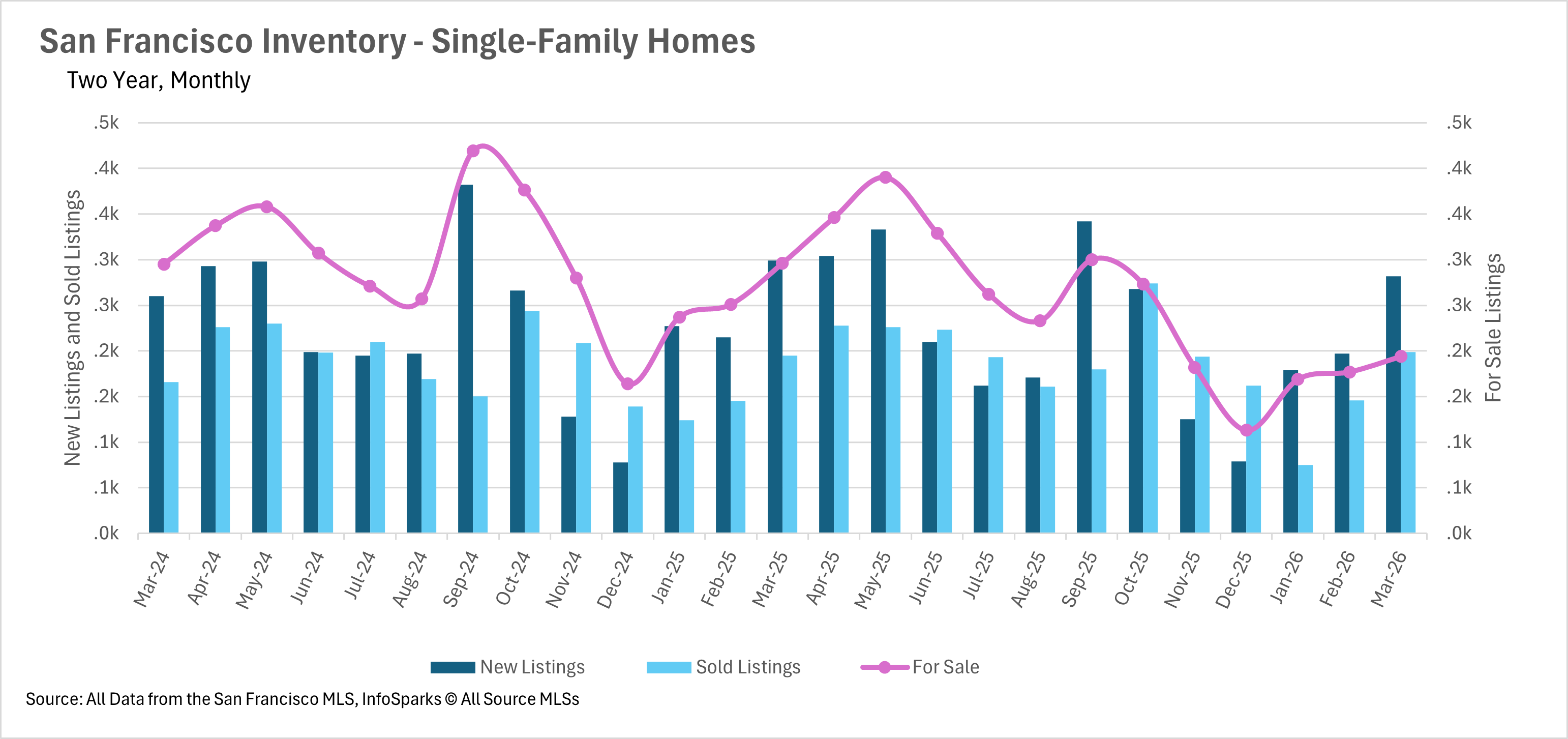

Existing home sales rebounded slightly from January, but remain below where they were at this time last year.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.