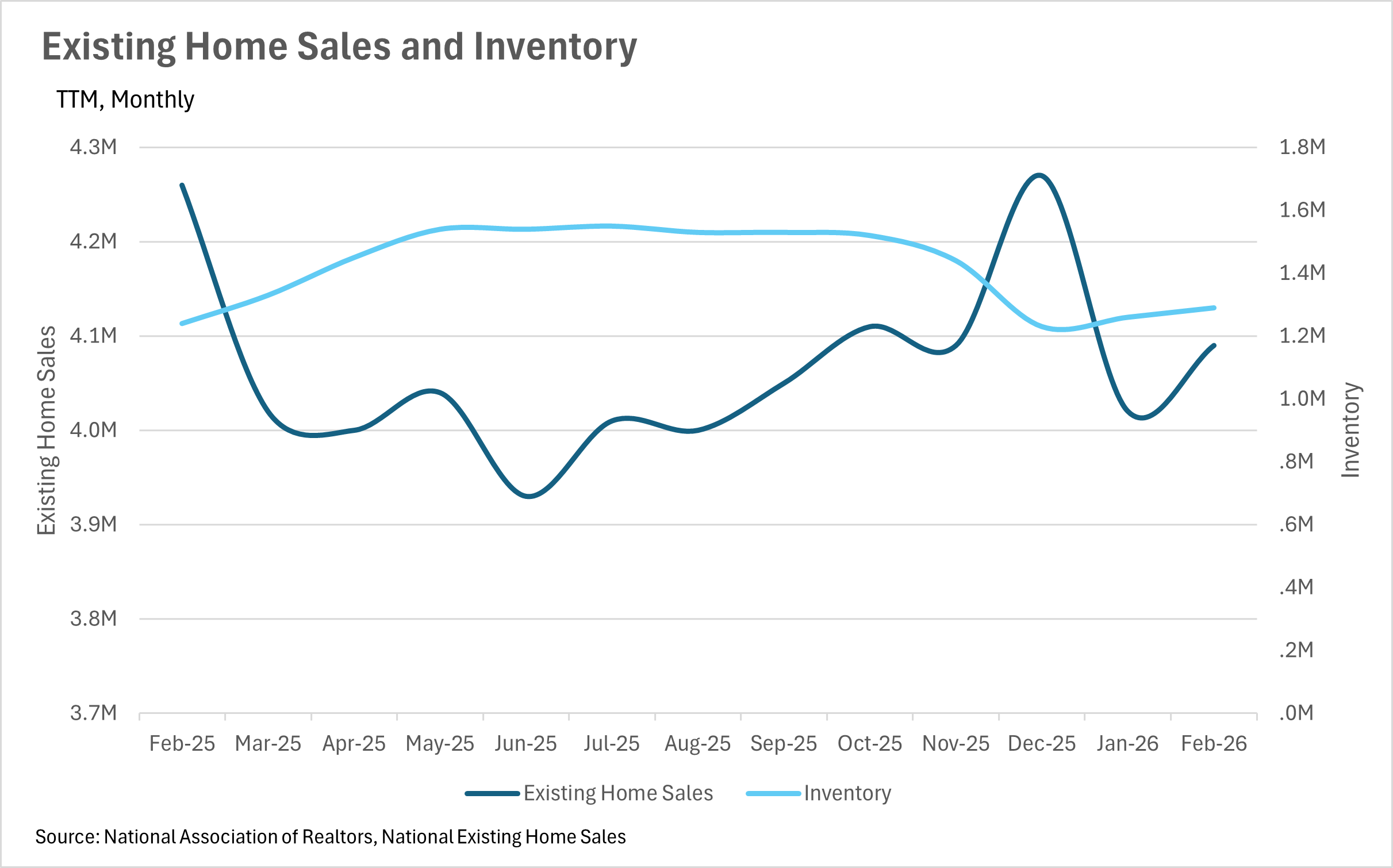

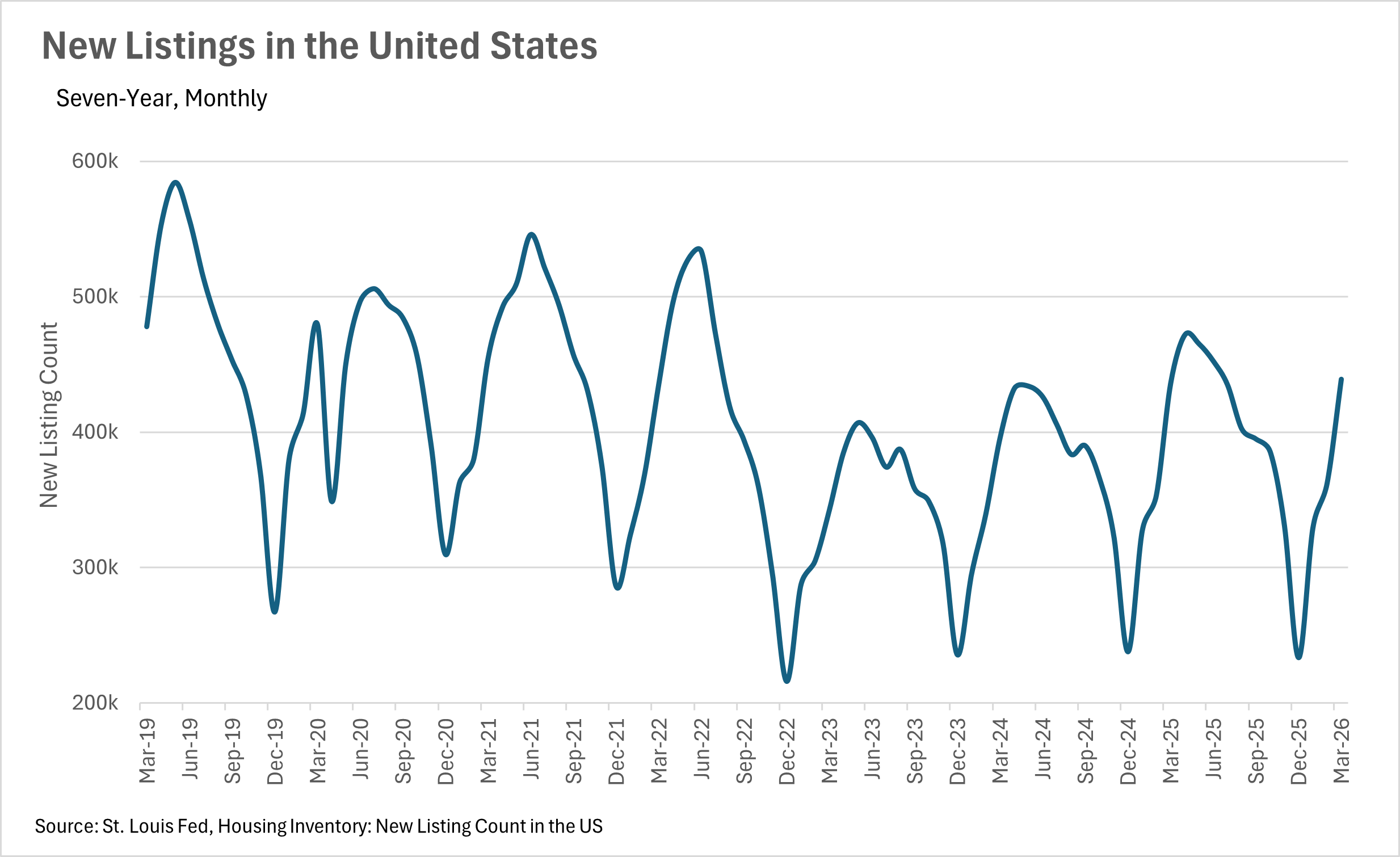

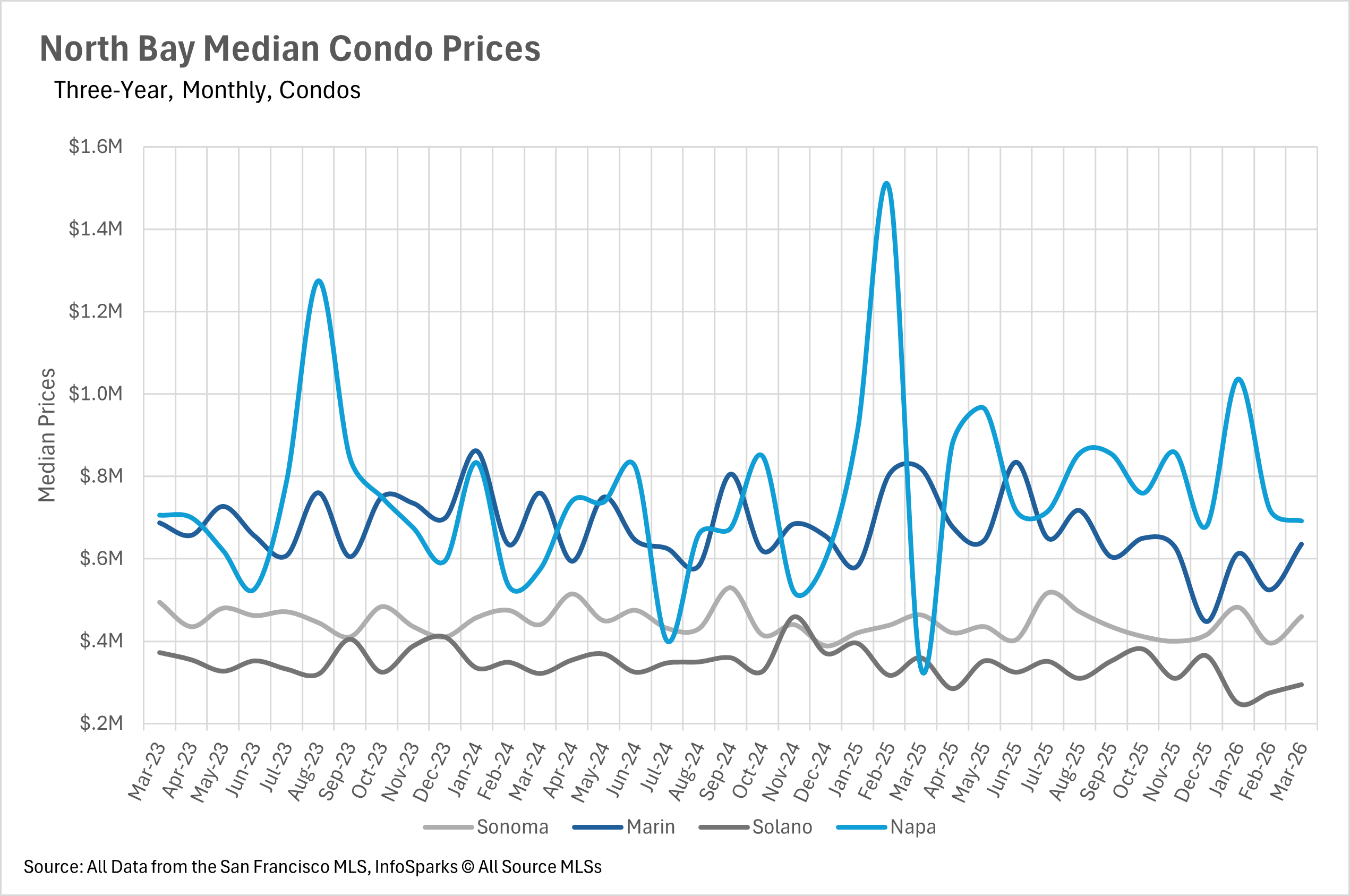

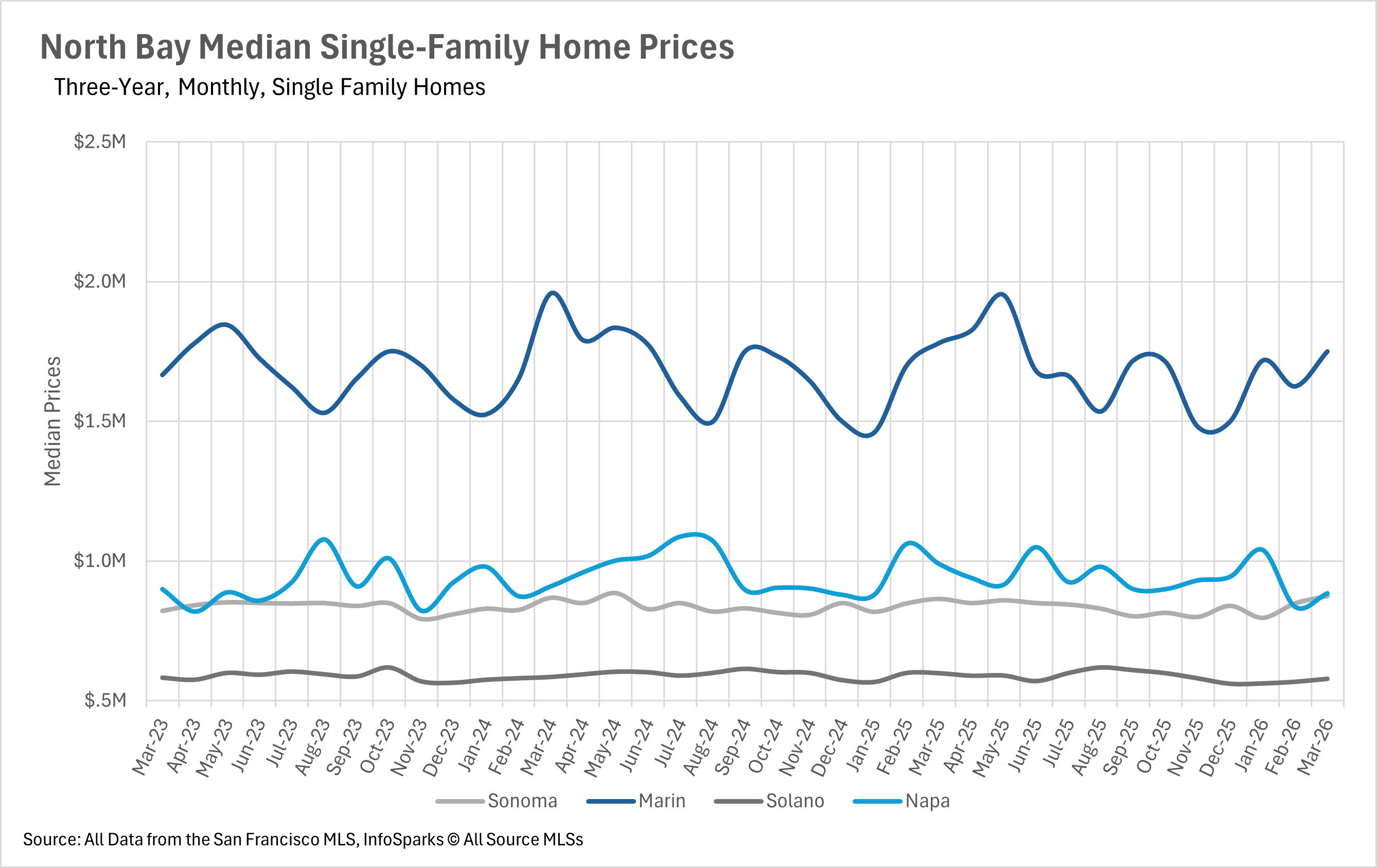

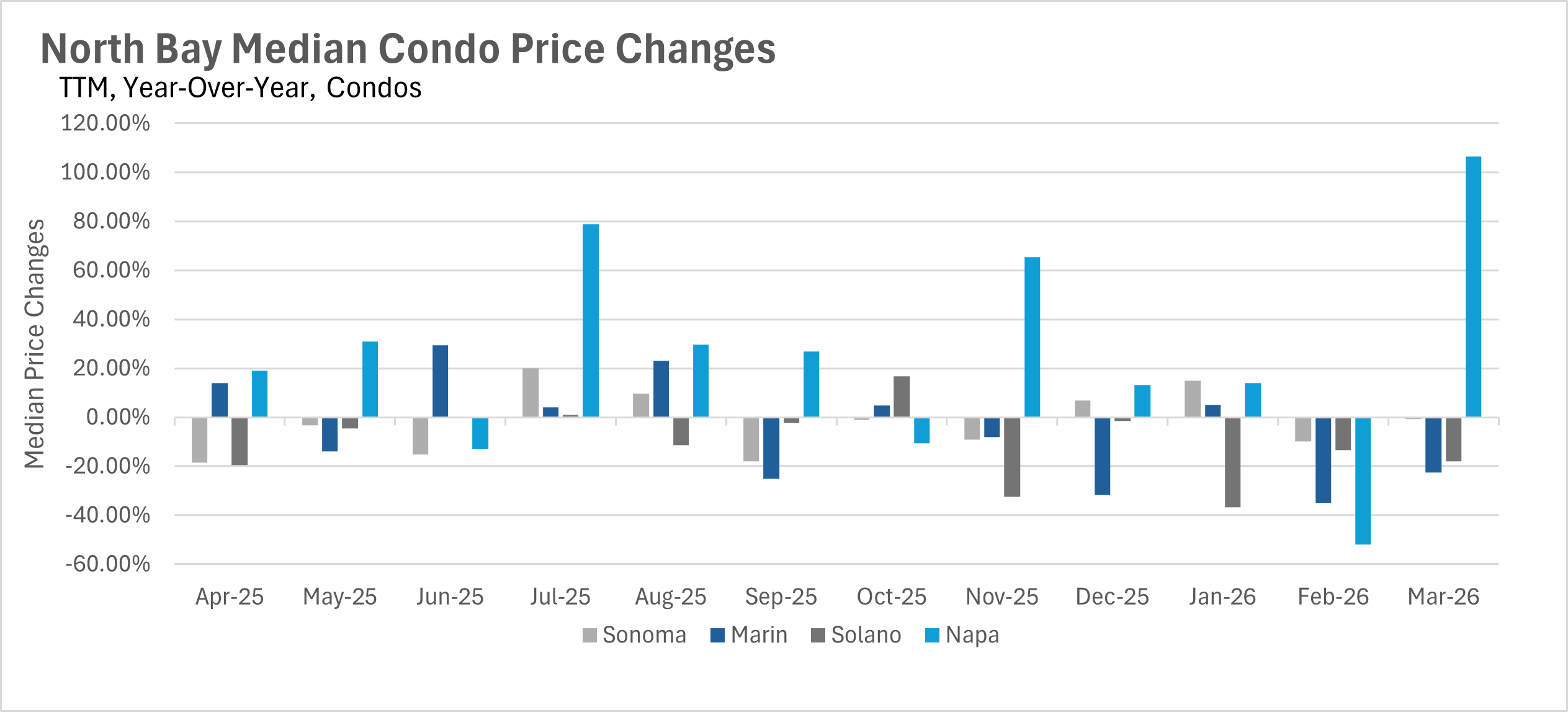

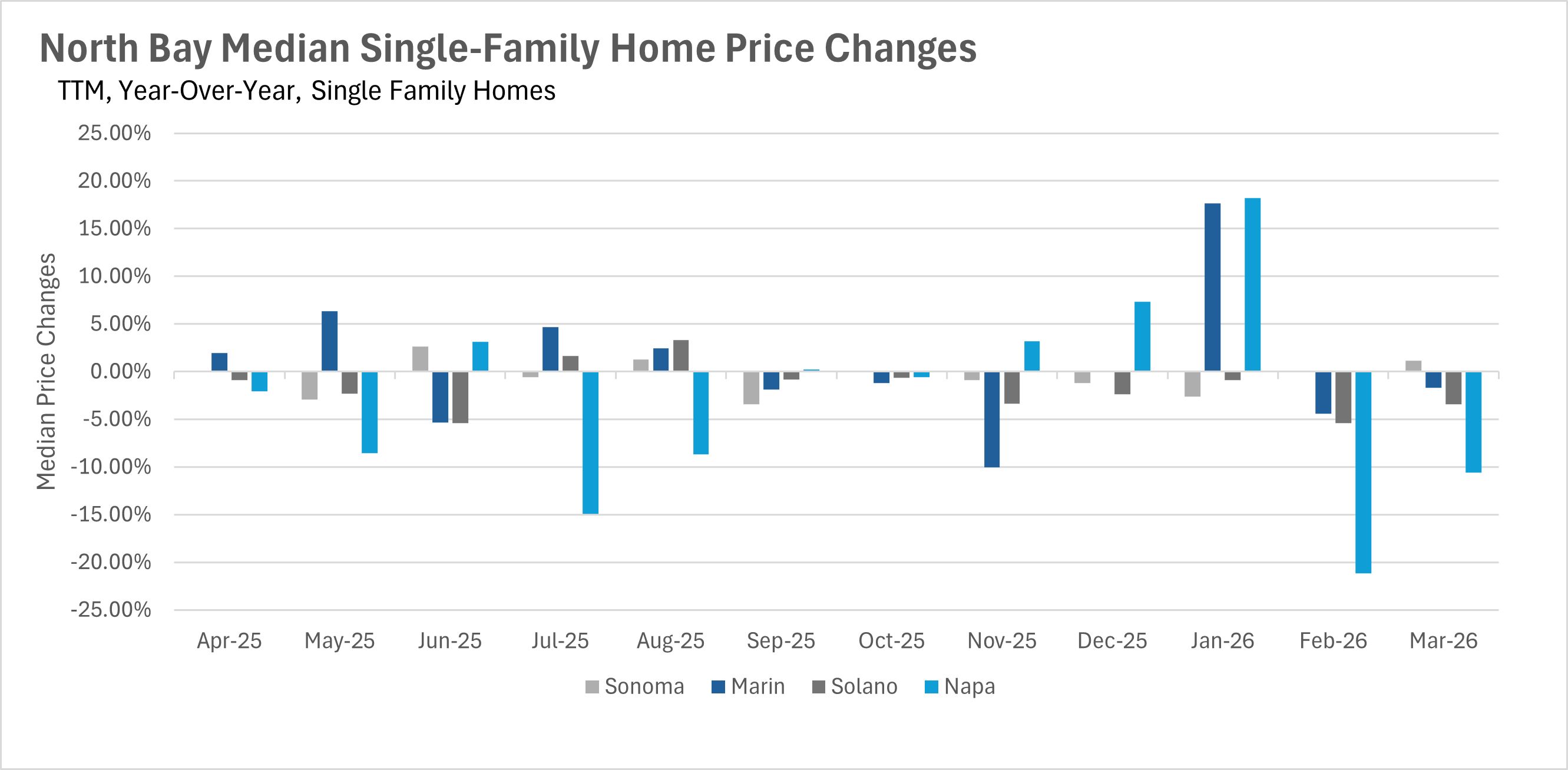

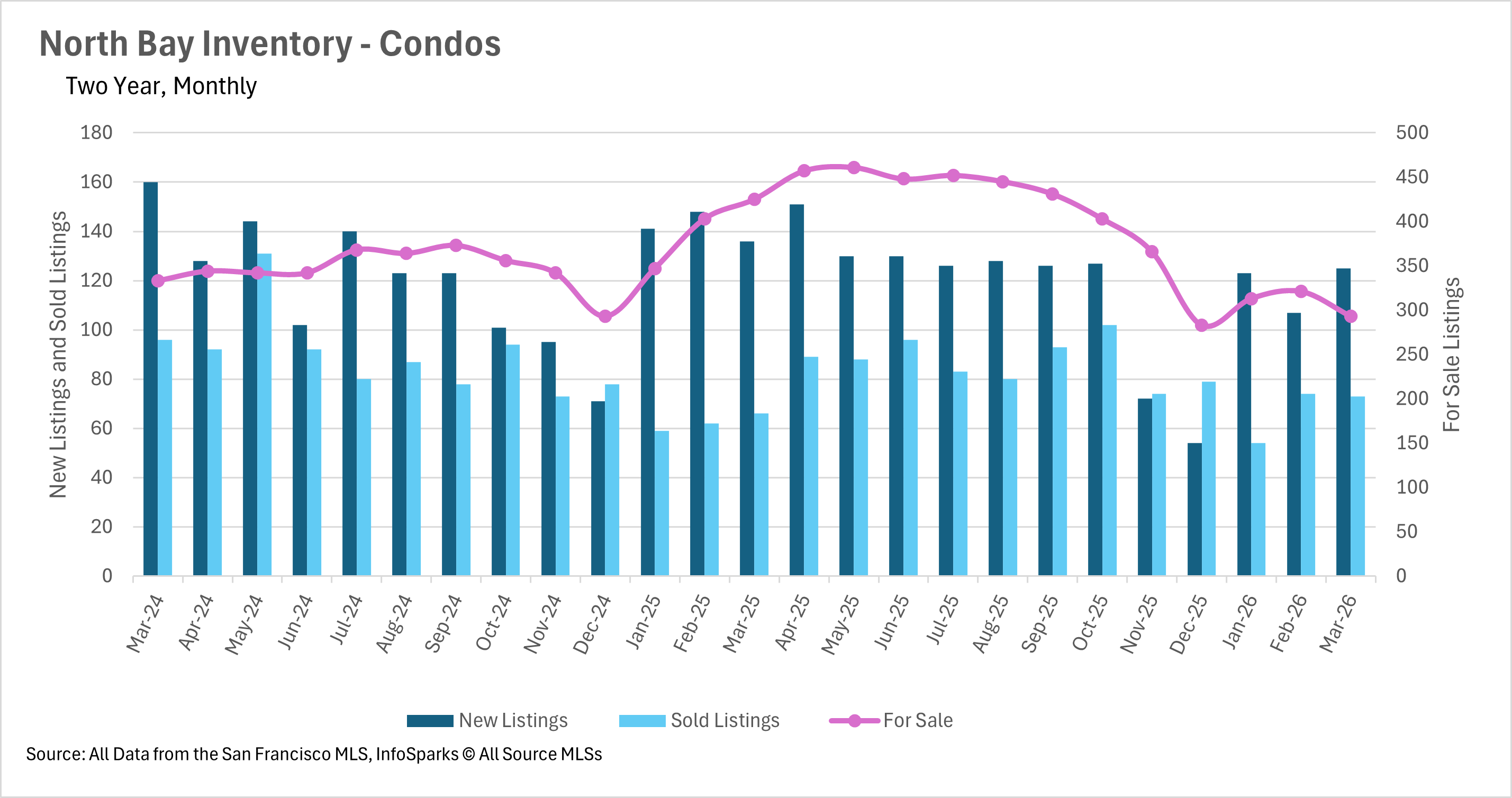

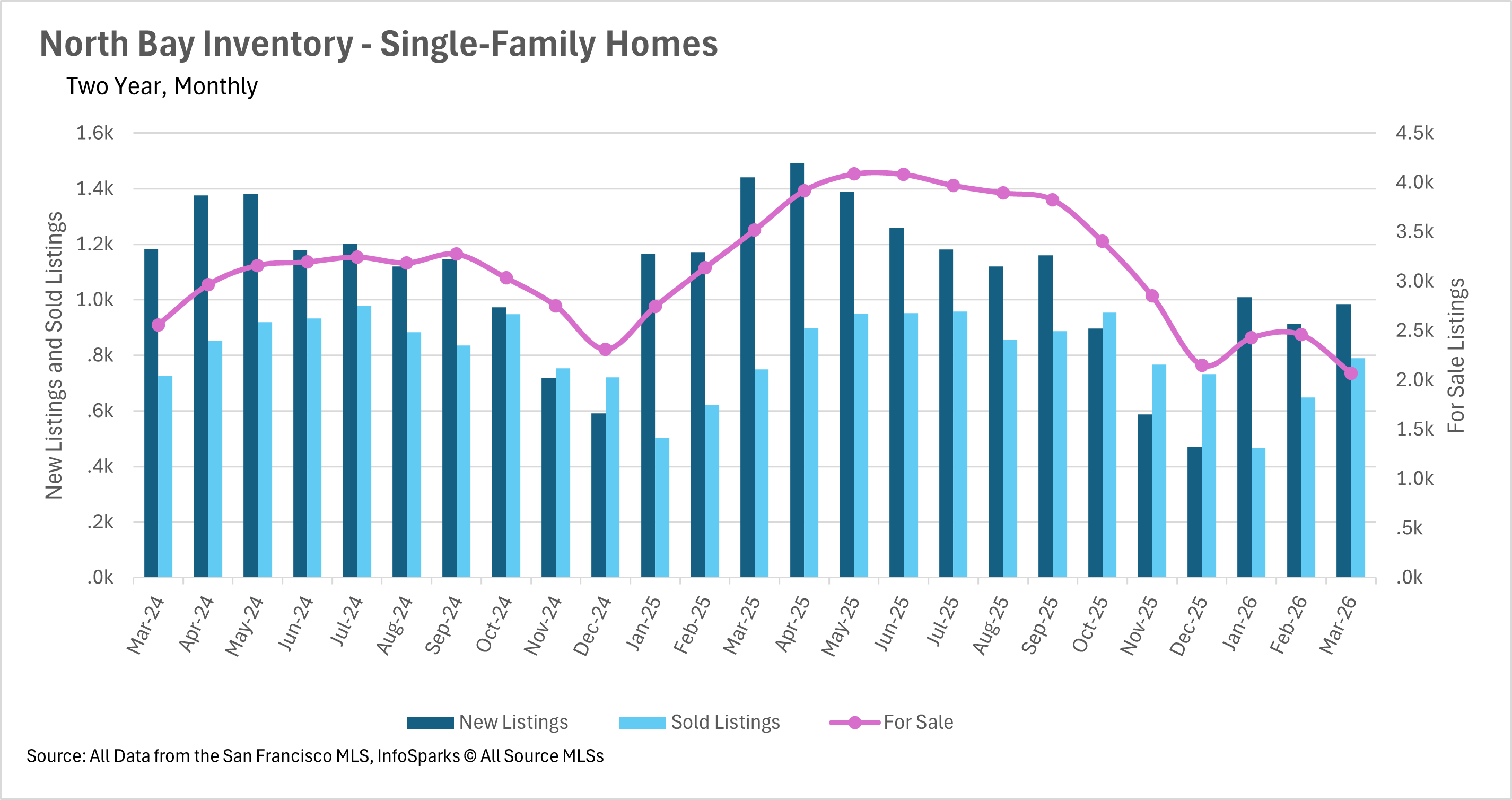

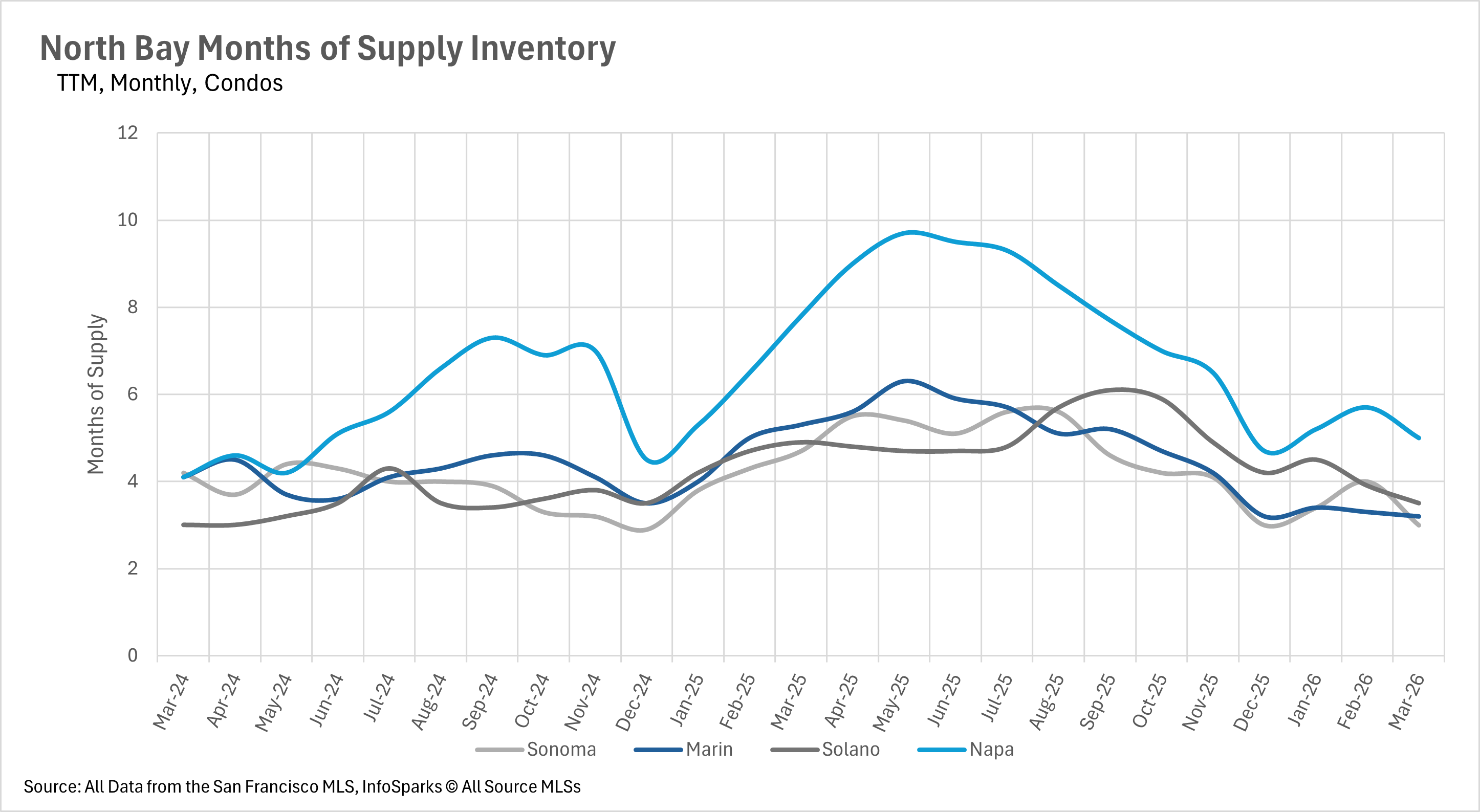

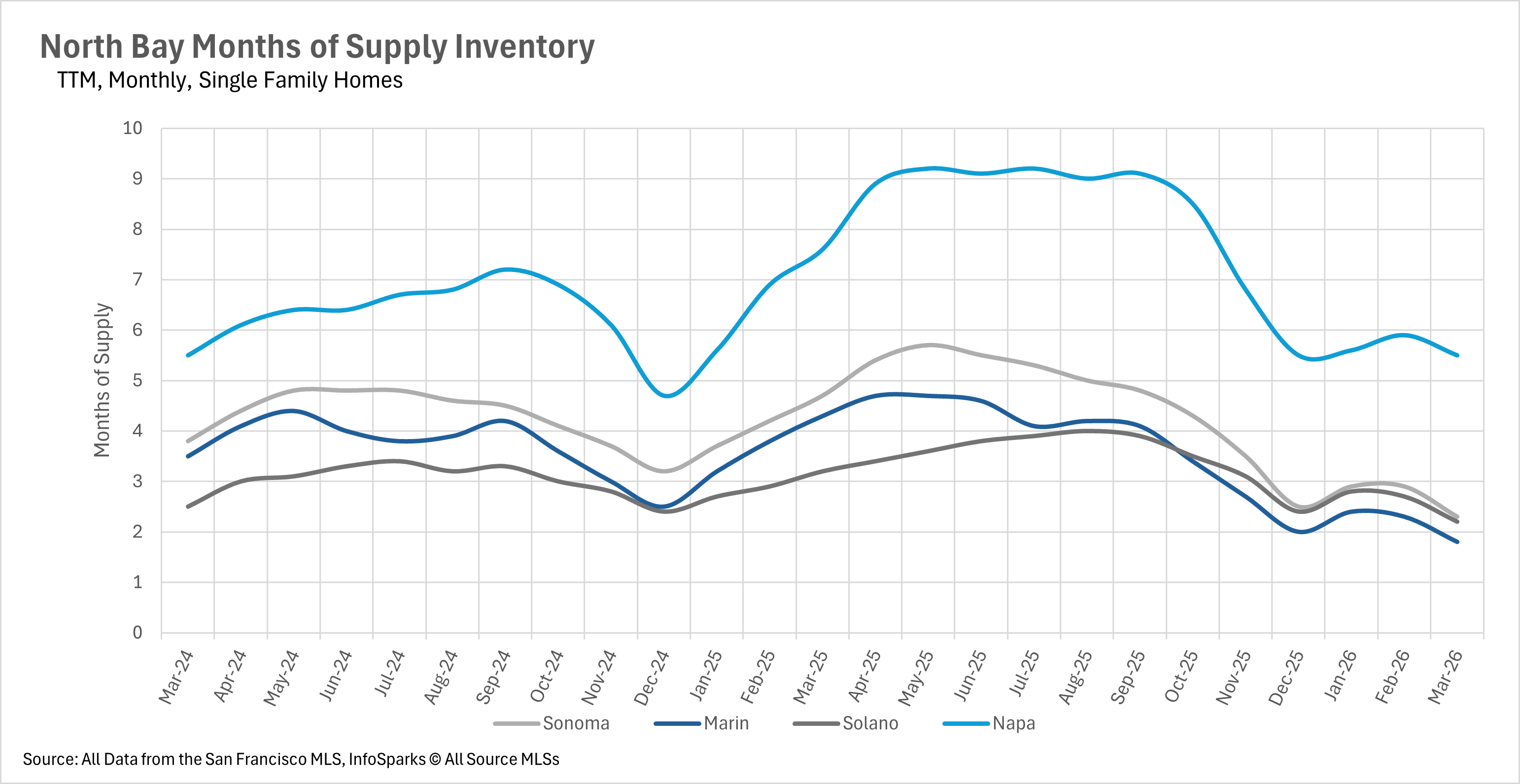

Inventory levels continue to climb modestly on a year-over-year basis, with new listings surging heading into the spring selling season.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.