See Your Home’s Value

This month, we take an initial look at the first half of 2020 in the context of the local, state, and national real estate markets. Since March, the pandemic has brought us largely into our homes. Many of us have learned through the last several months that the quality of our dwellings greatly affects the quality of our lives. Our time in our homes will likely continue as Governor Newsom began scaling back California’s reopening on July 13 without a stated end date. During uncertain times like these, we continue to provide you with the most up-to-date market information, so you, our clients, feel supported and informed.

- Key News and Trends in July: Across the United States, COVID-19 cases continue to rise as both the economy and rental markets struggle. Meanwhile, pending home sales set records nationwide.

- July Housing Market Updates: San Francisco’s single-family home prices climb to their highest levels in over two years due to a steep drop in new listings alongside growing buyer demand.

Key News and Trends in July:

Data released on July 8, 2020 by Johns Hopkins University, showed that California was among 12 states with record-high, seven-day averages for daily new coronavirus cases. California also saw a surge in the number of hospitalizations. Gavin Newsom said at a news conference on July 8th that over the previous two weeks, the state has seen a 44% increase in hospitalizations and a 34% increase in intensive care unit (ICU) admissions.

In our May newsletter, we cited the same sources, which predicted that nationwide hospitalizations would be near zero by July. Now, experts predict that hospitalizations will continue to trend upward as we head later into the year. This will prolong some of the negative economic effects that the pandemic has already induced—nearly one in every six California workers is out of a job, and many others face reduced hours.

The rental property market is one sector of the economy feeling the effects of the prolonged pandemic. As reported by Curbed,

the rent for one-bedroom apartments in San Francisco fell 9.2% year-over-year in May. Curbed also believes that rent drops may be even higher since some landlords conceal price drops in lease specials like six weeks of free rent for new move-ins. Compared to homeowners who have access to useful financial support tools, namely refinancing at a lower rate and forbearance, lowering rents is difficult to do because rents can only be renegotiated if the landlord is willing. While San Francisco recently

extended the moratorium on rent evictions during the pandemic, the protections do not include rent cancellation; renters will still owe missed rental payments within six months. In general, renters are the first to experience housing burdens because they have much smaller savings and are more vulnerable to income shocks. As reported by UC Berkeley in April,

roughly 50% of likely-impacted renter households were already struggling with rental cost burdens before the COVID-19 crisis took hold. Although the decline in renters will not necessarily impact single-family homes and condos immediately, a persistent exodus and subsequent rent price declines could slowly make its way to homeowners’ equity. One way to value a home is to calculate the net present value of rental income were the owner to rent the property.

Meanwhile, both state and local housing markets remain resilient, partly because of healthy home sales in an undersupplied market, which is a phenomenon also seen nationwide. On June 29th, the National Association of Realtors (NAR) reported that pending home sales mounted a record comeback in May, rising 44% and chronicling the highest month-over-month gain since the index’s inception in 2001.

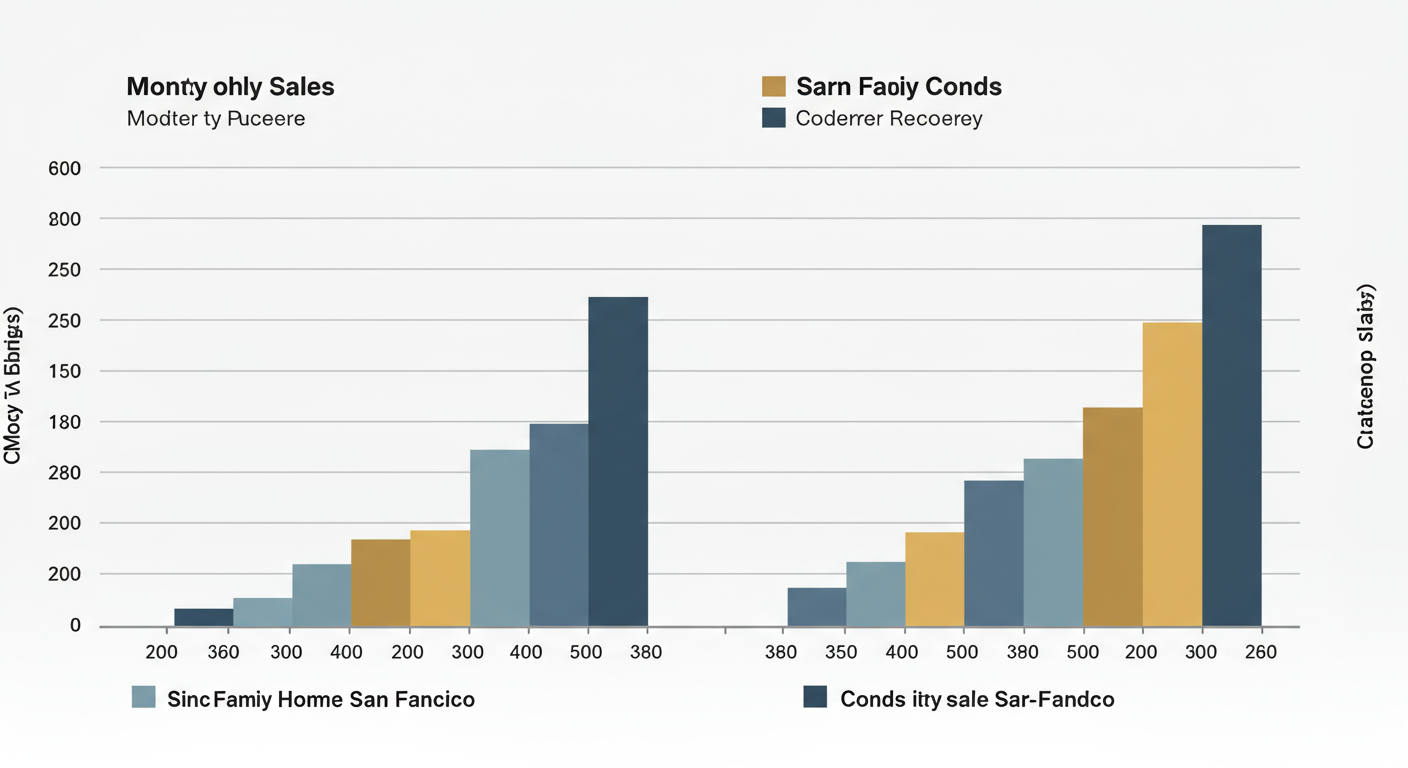

June Housing Market Updates for San Francisco

In the month of June,

single-family home prices rose to their highest levels on record. The condo market also picked back up.

Looking at the yearly price data, single-family homes were up 3% from this time last year, while condos were down 7%.

San Francisco’s prices tend to be buoyed by a lack of supply compared to demand. As we continue to report, the biggest impact has been on sellers who face logistical challenges in selling their homes, such as the safety of inviting prospective buyers into an occupied home. The majority of sellers are simultaneously buyers themselves, which means they are navigating two transactions. For this reason, sellers have taken a tempered approach to enter the market.

Unfortunately, COVID-19’s rise seems to have amplified buyer and seller tendencies. Weekly new listings for both single-family homes and condos continued falling in June nearly back to the levels at which they were in late March and early April.

Meanwhile, buyers have been more aggressive. Matt Levin, head Housing and Data journalist for

CalMatters, argues that prolonged record-low inventory coincided with the huge millennial generation reaching the home-buying age. Many of these hopeful and credit-worthy home buyers built up the savings to meet tight lending standards. These home buyers still want access to homeownership. Additionally, buying before the pandemic had its own set of risks, especially in San Francisco, such as entering into a bidding war or paying as much as 5%–10% over list prices for homes or condos. Arguably, these risks were greater than the risks today associated with committing to a mostly virtual transaction.

To address Levin’s point, San Francisco’s homes under contract continued to trend upward.

We can also take a look at home sales—the result of homes under contract that close within 30 days—on a monthly basis, while also comparing them to last year’s numbers. Sales are down, but they are down much less for single-family homes than most people may expect in this economic climate (-14% year-over-year). Sales for condos seem to be recovering as well, but they are still far from where they were last year.

Together, fewer listings and higher sales move inventory levels back down. Measured weekly, we can see the levels for both single-family homes and condos trending lower every week in June.

Months of Supply Inventory (MSI), the measure of how many months it would take for all the current homes for sale on the market to sell at the current rate of sales, has an average of three months in California. A number lower than three means that buyers are dominating the market and there are relatively few sellers; a higher number means there are more sellers than buyers. In June, the MSI for single-family homes fell well below the three-month average and now heavily favors the sellers once again. The MSI of condos was not as tight; however, it was low enough to insulate prices.

Record prices indicate that there are not many bargains on the market. However, June’s sale-to-list ratios—which compare the prices buyers pay to the original list prices of homes—suggest that buyers are also not paying large premiums due to bidding wars. The chart below illustrates the price that the average San Francisco buyer negotiated, above or below the list price, to put a property under contract. In June, both single-family homes and condos sold in line with the original list price.

Lastly, we look at the percentage of homes with price cuts. In San Francisco, 16% of single-family home prices were cut, up from only 7% in April. Meanwhile, the percentage of condos with price cuts fell. In our May newsletter, we reported that many sellers were reluctant to lower their list prices, asserting that the failure to sell was due to the pandemic rather than an overpriced home. For single-family homes, at least, some sellers may finally be willing to reduce their prices.

In summary, as we discussed in previous newsletters, the fundamentals of the housing market were strong before the global economy stalled, and they have continued to show stability. The prolonged pandemic will continue to cause fluctuations in the market, some of which can be measured weekly. It is now more important than ever to have access to the advice of real estate professionals.

Looking ahead to August, we anticipate the undersupply in housing to continue. The COVID-19 spike in California and across the country has created economic and personal unease. Sellers tend to be timider during this time while buyers are more aggressive, feeding into the undersupply and lifting home prices. As more supply becomes available, there could be a correction in the market, but we do not believe that is likely through the summer months.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals is happy to discuss the information we have shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.